-

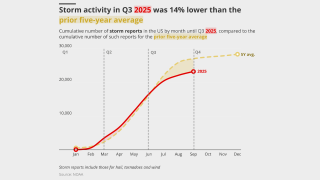

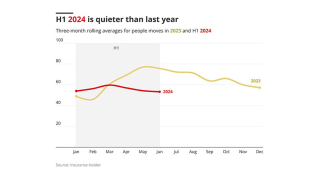

Despite a rocky H1, 2025 insured losses from nat cat events may not surpass 2024 levels.

Despite a rocky H1, 2025 insured losses from nat cat events may not surpass 2024 levels. -

The class offers affirmative coverage for gaps in traditional insurance policies.

-

Continental composite carriers aim to smooth volatility with new initiatives.

-

Several airlines are understood to have come to market early.

-

According to McKinsey, the projected spending on data centers is expected to hit $6.7tn by 2030.

-

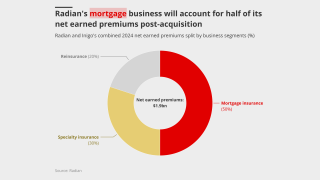

The deal will be watched closely by Radian’s handful of similar peers.

-

Small modular reactors are increasingly viewed as a means of meeting surging energy demand.

-

After losing in the High Court, insurers pin their hopes on the Court of Appeal.

-

Despite formation of Gabrielle, there is "a very high probability" of a below-average season.

-

Part four looks at how the talent landscape will shift in response to AI introduction.

-

The low degree of overlap between the combining portfolios benefits both parties.

-

Organisations were challenged to address systemic DEI failure rather than play “word salad” with labels.

-

Property remains the dominant line, accounting for nearly 30% of total London premiums.

-

Plaintiffs allege that manufacturers and retailers have broken environmental laws.

-

From aviation claims to retention challenges, underlying dynamics will take time to play out.

-

There are concerns that repeated delays could lead to market disengagement with the process.

-

Blackstone-style capital seeking to get closer to source is a net negative for reinsurers.

-

Cedants target methods of reducing pressure on earnings as reinsurers chase growth.

-

Apollo most recently received in-principle approval for Syndicate 1972.

-

The aviation market may prove an outlier following a disastrous year of loss activity.

-

The private ILS segment took losses from LA wildfires and Mid-West severe convective storms in H1 2025.

-

Reinsurers and their cedants are feeling their books are in better shape, although the market is still uneven.

-

The carrier M&A cycle has started and reinsurance is a segment where acquisitions work better.

-

The post-disaster reinsurance start-up model is changing.

-

Terms are expected to hold, underpinning the stronger recent performance of reinsurers.

-

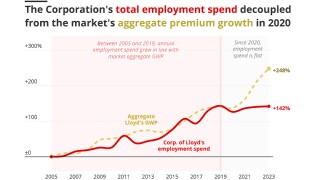

Maintaining underwriting discipline was central to the Corporation's messaging.

-

The cycle-turn M&A story continues with strategic buyers to the fore.

-

Cyber reinsurance supply has continued to outstrip demand during 2025.

-

The Japanese carrier faces integration challenges to make a success of the deal.

-

City firms have introduced perks of extending working from home periods and half days in summer.

-

Insight into the state of the insurance M&A market, powered by this publication's deal database.

-

Rates are bottoming out, but ample capacity is still preventing a hardening market.

-

The Japanese company announced the $3.5bn deal today, three months after the Bermudian completed its IPO.

-

Submission volume is up 10%-20%, according to sources.

-

A notable uptick in attendance underpins the value still placed on the iconic trading centre.

-

The mid-year renewals point to mounting pressure on reinsurance pricing.

-

Part III of our series looks at where AI is being integrated into underwriting departments.

-

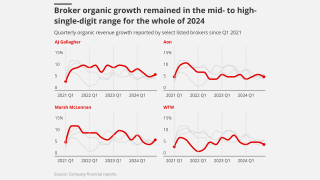

Top line grew across all carriers even as pre-tax profits dipped.

-

As rate reductions present headwinds, firms are expected to moderate expansion.

-

Brokers turn to harder classes, innovation, commissions and tech to soften the blow.

-

Market leaders Atradius and Coface have both received in-principle approvals for a Lloyd’s syndicate.

-

However, group organic growth among public brokers has slowed to pre-pandemic levels.

-

Emerging lawsuits and expanding loss triggers are giving rise to potential claims under a range of policies.

-

Cat portfolios generally grew, but casualty approaches varied.

-

In part II of our series, we look at where AI is being integrated into claims departments.

-

Insight into the state of the insurance M&A market, powered by this publication's deal database.

-

Improved book value, a healthy CoR and disciplined underwriting mark the CEO’s time at the helm.

-

The impact on the (re)insurance market has been muted due to its strong capital position.

-

A look into how the insurance industry is using AI and where practical gains are arising.

-

Despite steep rate hikes, premium volume has held steady as players such as SpaceX self-insure.

-

Questions remain over regulatory touch, capital requirements and tax benefits

-

Continued Apax and Carlyle support will give PIB time to differentiate its business.

-

The business is one of the first to sell in this round of Lloyd’s M&A.

-

Sources said the downstream energy market is unlikely to turn a profit in 2025.

-

The challenge now is balancing top-line growth with underwriting discipline amid falling rates.

-

The three months to June included a cluster of Guy Carpenter exits.

-

The aerospace, energy and marine markets all sustained multiple significant losses in H1.

-

Green hushing is on the rise as Trump rows back on climate initiatives.

-

Insight into the state of the insurance M&A market, powered by this publication's deal database.

-

Although US pricing is improving there is pressure in other geographies.

-

Hannover Re’s CEO is lowest paid among peers, despite their pay growing 77% since 2015.

-

The investment comes amid expectations of a new cycle of deals.

-

Some segments are moving faster than anticipated, but overall, it remains a mixed bag.

-

Working out ROI on sponsorship deals is difficult, but the sport is beloved by insurance brands.

-

The protection gap is calling into question the relevance of the insurance industry.

-

Who will buy the swathe of PE-backed Lloyd’s firms coming to market over 2025-26?

-

Future claims handlers could be "bionic adjusters” empowered by technology.

-

The increased tariff on China trade could drive up the loss quantum on the SharkNinja recall and others.

-

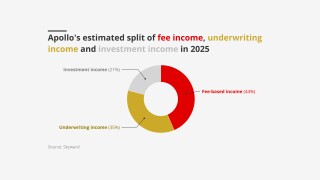

Analysts were interested in the potential for fee income from the retail division.

-

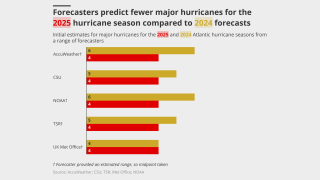

This year is predicted to be an above-average season, like 2024.

-

Lloyd’s maverick syndicate produces impressive results, but questions remain over succession.

-

Insight into the state of the insurance M&A market, powered by this publication's deal database.

-

Broker facilities and increased US domestic appetite are accelerating the softening.

-

As with 2024, pricing pressure has been most acute on top layers.

-

P&C combined ratios were higher than Q1 2024, and wildfires impacted Hannover Re most.

-

Delegates welcomed the FCA’s red-tape cut, but said more is yet to come.

-

Soft conditions have led to “less acute" underwriting discipline, sources said.

-

More players are looking to the class in a bid for top-line growth.

-

Sentiment at the ILS Connect event hosted by Insurance Insider ILS was generally positive.

-

Beazley, Hiscox and Lancashire all grew in Q1 despite widespread rate decreases.

-

We assess the Bermudian’s standing amid waning investor sentiment and economic uncertainty.

-

Insight into the state of the insurance M&A market, powered by Insurance Insider’s comprehensive deal database.

-

Risk managers at last week’s Axco summit said interconnected global risks require flexibility.

-

As the next generation of Names comes to the fore, advisers urge simplification.

-

Insolvencies caused by the tariffs could also cause increased losses

-

Fridays in the office will be the toughest nut to crack.

-

Sources expect it to be a couple billion-dollar insurable market.

-

Due diligence is essential to make sure incubators are backing winners.

-

Aegis 1225 jumped from fifth place last year to become the most profitable syndicate of the last decade.

-

Trade credit and marine are among the lines facing direct impacts amid a broader inflationary challenge.

-

Despite a softening market, carriers still have belief in their profitability, sources said.

-

Insight into the state of the insurance M&A market, powered by Insurance Insider’s comprehensive deal database.

-

Sources said extending coverage to Gen AI may be difficult and unnecessary.

-

The first quartile contracted on the back of Beazley 2623’s GWP reduction.

-

Reinsurers fended off 20% cuts, but wildfires pleas failed to hold pricing flat.

-

Last year, nearly two-thirds of Lloyd’s syndicates reported a deterioration in combined ratio.

-

Insurer appetite for facilities is not just about top line, it is also a hedge against disruption.

-

In the first part of this series, we explore how smart-followers are mixing up their strategies.

-

The market took a higher share of hurricane losses and couldn’t cut its acquisition costs.

-

Sources warned some property XoL books are already running 50% loss ratios.

-

The proportion of women in lead underwriting roles still trails other leadership positions.

-

Some of the Big Four are slowing growth as the market softens.

-

The market improved on attritional losses in 2024 – but slowing rate growth raises queries over top-line momentum.

-

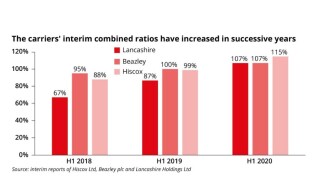

Hiscox, Beazley and Lancashire all reported top line growth, but ROEs dipped in an active wind season.

-

Sources warned of the erosion of underwriting margins after a string of strong years.

-

Two major claims have prompted underwriters to question the sustainability of double-digit rate decreases.

-

Some firms are broadening their M&A net in light of PE firms showing more restrained appetite for intermediaries.

-

Lloyd’s CEO pay is lowest compared to major LSE-traded specialty insurers by a considerable margin.

-

The transactional liability class faces a string of potential losses, especially in the contingent segment.

-

Cedants could choose to retain more as cross-share sell-offs boost their capital.

-

Social inflation and larger vessels are making multi-billion losses more likely.

-

A higher loss quantum will put a greater burden on retro programmes.

-

With another year of underwriting profits banked, the ‘Golden Age’ isn’t over yet.

-

Deteriorating CoRs, GWP growth and fears over wildfire impacts were common themes.

-

Settlements could reduce seized aircraft quantum to the mid-single billions of dollars.

-

Newer swing products offer an alternative way to deal with escalating awards.

-

Underinsurance, total loss claims, and high property values have impacted loss estimates.

-

As the market turns, balance sheet M&A is becoming a more appealing option.

-

Single-digit organic growth, robust casualty pricing and tapering margins were all key trends.

-

With Atrium marking another case of potential bifurcation, where is the natural home of risk?

-

These businesses are expecting more premium growth than the wider market this year.

-

Secondary perils accounted for 65% of global insured losses in 2024.

-

A combination of mandated days and soft pressure is driving up EC3 attendance.

-

The California fires will test post-2018 treaty revisions – and reinsurers’ nerves.

-

Loss assessment is at an early stage, but senior sources suggested the claim could surpass $1bn.

-

In the food and beverage market, rates are falling by an average of 3%-4%.

-

Market softening means exploiting hardening niches is the name of the game.

-

Underwriting oversight is top of the agenda for some, whilst others prioritise progress on tech and operations.

-

High-net-worth binders and treaty exposures will bring significant claims to Lloyd’s writers.

-

We explore the strands of the Lloyd's leader's six-year tenure, moving from remediation to growth mode.

-

Carriers rushing headlong into gen AI without considering its ESG implications could face costly complications down the road.

-

The path to Howden’s new era is steep – but the opportunity is vast.

-

In part two of our 2025 outlook, we explore the drivers of carrier M&A and recreating the ESG agenda.

-

Certain new and old themes will re-emerge this year as the balance of power shifts.

-

Reinsurer appetite largely outweighed demand at 1 January.

-

As 2024 draws to a close, we reflect on the events of the year for the London market.

-

Concern over rate adequacy remains, but reinsurers are delving deeper into data rather than walking away.

-

As 2024 draws to a close, we reflect on the events of the year for the London market.

-

High deductibles, tighter underwriting and lack of flood cover meant lower claims figures.

-

Insight into the insurance M&A market, powered by Insurance Insider’s deal database.

-

Reinsurer appetite for aggregates begins to creep back in.

-

Overall, reinsurers accepted that rate cuts were still leaving them with strong margins.

-

Annual growth in demand for tax insurance ranged between 25% to 40%, sources said.

-

First-quartile 2023 performers will contract capacity by 5% in aggregate next year, according to our survey analysis.

-

Lower inflation and a softer market outlook tempered aggregate growth expectations.

-

Marine and energy were the busiest lines, driven by high competition for talent.

-

A resurgence in IPO activity may help provide new business for underwriters and reduce competition.

-

Lloyd’s has taken around 6% of aggregate US hurricane losses in recent years, and disclosed estimated net losses from Helene and Milton of $1.8bn to $3.4bn.

-

The 2024 hurricane season stayed within predictions for high activity but lacked market-moving events.

-

The market’s dearth of third-party managing agents is a source of tension among young syndicates.

-

Sources agreed that to achieve growth, the focus is shifting from the US to SMEs in Europe.

-

Helene losses were spread wider than initially suggested, in contrast to Milton claims.

-

The 2024 event saw 80 speakers address an audience of over 350.

-

Growth vs discipline, smart follow and M&A mean 2025 will be a mixed bag for London.

-

-

Fidelis 3123 and NormanMax 3939 were the first syndicates to adopt modifications.

-

The D&F market now expects 2025 renewals to be flat to down 5%

-

The A&H market had improved performance between 2020 and 2023.

-

The loss of premium income from Glencore is expected to add to competitive pressures running up to 1 January.

-

Credit insurers may need to adapt their business mix, client base and types of deals underwritten to stay relevant.

-

Achieving profitability is increasingly challenging in the volatile but historically lucrative market.

-

Risk managers are increasingly concerned about insurability.

-

Some reinsurers are considering frequency protection products.

-

Assuming Munich Re takes roughly a 3% market share of hurricane losses suggests a ~$20bn industry loss for Helene.

-

A canvassing of the market showed some bifurcation on the necessity of a government backstop.

-

There has been some strategic withdrawal of capital for younger syndicates.

-

A more residential-skewed loss would impact Lloyd’s carriers in treaty where market share is lower.

-

Milton made landfall south of Tampa Bay at Category 3 on Wednesday night.

-

Setting aside the storm’s greater potential insured loss scale, the flood risk implies greater exposure.

-

Increased interest follows ratings agency upgrades of Lloyd’s paper.

-

Most sources noted expectations of a $50bn+ event, but the range of outcomes is huge.

-

Space insurers are running at a near-200% loss ratio after booking losses of over $1bn in 2023.

-

Many insurers have cut back lines in Lebanon, although larger insured sums are at stake in Israel.

-

Sources expect significant loss amplification in the claims that will come from Georgia, the Carolinas and Tennessee.

-

The Category 4 event will highlight the impact of recent market hardening.

-

Loss-free accounts are expected to be oversubscribed by as much as 140%.

-

This is the first major update to the misconduct framework since enforcement powers were introduced in 2005.

-

M&A levels have increased 23% year-to-date compared to 2023, according to Gallagher Specialty.

-

Construction rates remain stable with some talk of potential softening.

-

The marine market is challenged by global warfare, supply chain breakdown and the complicated energy transition.

-

Treaty premiums have risen, while casualty premiums remain restrained.

-

Legal trends, the primary pricing micro-cycle and other factors all play into an opaque outlook.

-

Sources said that for reinsurers to meet this demand, they will need to get comfortable analysing and evaluating systemic and aggregate risk.

-

Negotiations are getting tougher, but overall market capacity is stable.

-

Swiss Re, Munich Re, Hannover and Scor each have challenges that will influence their renewal behaviour.

-

Reinsurers are high on their ‘redemption arc’. The question is – how long will it last?

-

The choice to build a reinsurance unit at arm’s length alleviates some financial strain.

-

Smart-follow is creating a third tier of provider – the “lead follower” – but broader efficiencies must be achieved.

-

Scor disclosed L&H troubles while Swiss Re continued reserving for US casualty.

-

Only 14% of board seats are filled by women, but directors at brokers tend to be younger than at managing agents.

-

The James River-Long Tail Re deal is the latest example of deal-specific investor capital.

-

However, some syndicates are planning more significant growth following hires or strategic shifts.

-

The regulator is considering changes that could penalise some international players.

-

The FCA’s aim is to reduce regulatory costs and increase the competitiveness of the commercial insurance market.

-

Hail remains the primary sub-peril dominating insured loss costs.

-

Lancashire was the only carrier to see double-digit growth in insurance revenue for H1.

-

A canvass of sources suggests that a $3bn-$5bn loss could tip the cyber market into unprofitable territory.

-

The market is warned to think about overall ecosystem interactions rather than “digitalising by stealth”.

-

Everest Re bucked a more general trend to keep cat exposure stable.

-

New capacity and increased competition is bringing rating levels under pressure.

-

The upside for brokers of a larger Lloyd’s is not necessarily clear.

-

US-listed brokers and carriers have generally continued to produce strong growth even in a transitioning market.

-

The cyber market should use the latest outage to start decisively taking action on managing cat aggregates.

-

Lloyd’s capital has several attractions to the MGA segment if it can manage the operational hurdles.

-

Market sources suggest that this will be a manageable loss, although at this early stage there are multiple uncertainties.

-

Resulting lowered expenses could feed into Lloyd’s ambitions of building a £100bn premium market.

-

Regulators are mulling reforms that could open the door to international independent brokers.

-

With Hiscox’s founders no longer at the helm, deal-making may be more achievable.

-

Two-thirds of insurance firms have been challenged about their resilience plans by the regulator.

-

John Neal’s expansion plan now has a five-year horizon, but deft execution will be needed.

-

Analysis of directors’ ages shows a shortage when it comes to the next generation of leaders.

-

Although talent movement in Q1 2024 was above Q1 2023 levels, personnel movement slowed in Q2 2024.

-

Quota share commissions are under pressure amid changing buying patterns.

-

Re-marketing of large fleets can result in double-digit rate decreases as carriers chase income.

-

Some 39% of respondents expect deal volumes to increase in the next 12 months.

-

Reinsurance sources say the pool targets the wrong aspects of Australian cat losses.

-

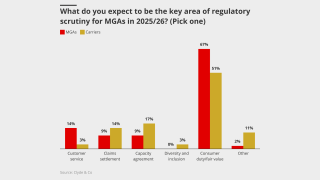

MGAs are looking hard at capacity arrangements for fear of regulatory action.

-

SCS caused global insured losses worth at least $8bn in the first quarter of 2024.

-

New business is arriving, but the captives market is not a priority target.

-

Underwriters fear that misleading statements about AI capabilities could result in claims.

-

The track record of smart-follow vehicles is still young, but the segment is gaining traction.

-

Sources said London should dodge the worst deterioration on US liability, but might not escape unscathed.

-

Forecasters have warned that a number of meteorological factors could make this year the most active on record.

-

Concerning hurricane forecasts are among the factors driving tighter reinsurer capacity.

-

The average risk adjusted rate increase is hovering at about 2% for clean business.

-

Combined ratios improved all around thanks to better pricing and a benign cat quarter.

-

The acquisition brings international M&A opportunities and a pipeline of London wholesale business.

-

Competition and broker pressure on rates is ramping up as London goes for growth.

-

The funding practice has led to a dramatic increase in claims amount, which in turn pushes up rates.

-

Property rates remain adequate, although price increases are tailing off.

-

Israel exposure has thrown inwards-outwards PV coverage mismatches to the fore again.

-

The market has advanced in sophistication but must tackle talent, tax and diversification issues.

-

A thriving competitive intermediary market is what keeps London fresh.

-

Sources approve of Labour’s plans around regulatory accountability.

-

Some firms are outsourcing their recruitment to tailor for a younger generation.

-

The US regulator faces litigation from both sides of the climate issue.

-

Recurring loss patterns have led to squeezed coverage, leaving clients exposed.

-

We explore the first stages of incorporation of GenAI into insurance, alongside the longer-term potential.

-

The recent Italian hail and Bernd losses show some companies are relying on outdated models.

-

This year’s analysis of profitability and volatility also includes an alternate view over five years.

-

Underwriters said there was some cause for concern around reinsurance coverage.

-

Transatlantic competition, rising valuations and price undercutting set a challenging scene.

-

In a departure from 2022 trends, fourth-quartile firms grew the slowest of all syndicates in 2023 at 8.1%.

-

-

We take a look at the outgoing CEO’s performance as he prepares to handover to CorSo CEO Andreas Berger.

-

Ariel and Blenheim were among eight syndicates moving into top underwriting quartile in 2023.

-

Work is still to be done on the investor proposition, expenses, and navigating a waning pricing cycle.

-

A claim on that scale would test the market in ways it has never seen.

-

AI was the hot topic throughout the InsurTech Insights event.

-

There is frustration in the market that remediation work has been squandered.

-

Hard-won profitability has given carriers room to salt away reserves.

-

Sources cited numerous issues with how collateral protection insurance was designed.

-

Hiscox, Beazley and Lancashire all delivered one-off capital returns while swerving casualty issues.

-

DDM is due to be removed as a core central service on 13 September.

-

On average, risks are being placed in a range of flat to up 5%.

-

Attention is fixed on how competition will impact pricing in H2.

-

CEO John Neal has ambitions to pull in more major insurers, E&S players and captives.

-

Rate increases have accelerated further after major losses in 2023.

-

Underwriters are pushing for rate rises, but competition is increasing.

-

Strong reinsurance results have absorbed long-tail reserve charges.

-

Investors are still keen on UK broking – but they may expect more for their money.

-

Fragile supply chains are driving up costs.

-

Being underweight US casualty gives the firm more room than peers to manoeuvre.

-

Convective storms cost more than ever, but activity was not exceptional.

-

Rates have fallen on the back of reduced deal flow in 2023.

-

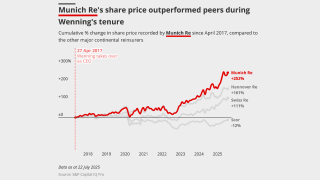

After HannoverRe announced a 2025 CEO transition, here is our last review on the company's successes and challenges ahead

-

Sources said that the market was not sufficiently profitable to concede ground on pricing.

-

The 1 January renewals featured a significant shift away from mainstay quota share and aggregate coverage, with examples including Axis and Brit dropping specific stop-loss covers.

-

Key market participants hailed the narrowing of the gap between PV insurance and reinsurance, however said that more still needs to be done to fix the market.

-

Prices are surging as a result of heightened risk but coverage remains readily available for shipowners.

-

In the second part of our themes for 2024 outlook, we explore how fear of missing out in cat reinsurance is still contrasting with an upstreaming of risk that is creating fallout for primary insurers, while momentum in facilitisation and ESG continues.

-

In the first section of our two-part outlook for 2024, we explore why macro-economic concerns are taking a step back, though casualty pricing micro-cycles highlight ongoing caution.

-

Reinsurers are making some adjustments to secure target signings but appetite to grow is finely balanced.

-

Well-priced top layer cat risk is in demand, leaving reinsurers watching the market carefully for any signs of decline.

-

The lack of momentum reflects on a general belief that underlying casualty business is well-priced for current years.

-

The PV market is facing yet another battle with reinsurers as they continue to restrict coverage, tighten definitions and exclude geographies.

-

Sources said that there was still rating adequacy in the market, but that further pricing falls would be unsustainable.

-

Howden was the most active acquirer as people-move activity peaked in Q2, this publication’s data showed.

-

Anticipations of a tug-of-war around a ‘flat to slightly up’ pricing renewal have indeed come to fruition.

-

Mass construction in remote locations is throwing up challenges around modelling exposures.

-

Sources said that with heightened geopolitical risks, pricing is already "much higher" than at any point in the last five years.

-

There are clear strategic advantages to the company’s London launch – but demand may not be as high as in the US.

-

The summit has been called the most significant for the industry to date, as there is a growing awareness of the value of insurance.

-

The voluntary carbon market reached $2bn in 2021, and is expected to grow to $10bn-$40bn by 2030, according to a report by Shell and the Boston Consulting Group published in January.

-

Growth opportunities at Lloyd’s no longer limited to top underwriting performers, Insurance Insider’s survey shows.

-

Growth slows from last year’s 20%, while QBE and TMK close the gap on Brit and Beazley.

-

The $10bn broking firm is progressing in its pivot towards specialty and international business, and an asset management model.

-

Rates are said to be doubling across the board as losses for 2023 top $1bn, resulting in a loss ratio of around 150%.

-

Cat losses were within budgets despite high levels of minor events.

-

Hamilton’s IPO share price came in at the lower end of historical trends observed amongst insurers that have missed their target range upon listing.

-

The mood at the association’s annual meeting is vastly more congenial this year, but challenges remain, particularly around long-tail lines.

-

The contingency market is monitoring the war between Israel and Hamas for potential loss activity, as well as keeping track on whether it has wider global implications for events, sources told this publication.

-

Last year’s APCIA took place during the post-Hurricane Ian stand-off, but despite the greater calm and certainty surrounding the run-up to this year’s 1 January renewal, there are several key themes to be debated at the event.

-

The number of female CEOs, CUOs, CFOs, MDs or board members has hardly changed in the past 12 months.

-

With US third-quarter reporting season being well underway, the results so far highlight further runway for the hard property E&S market.

-

Reports show that the combined use of supply chain exploitation and data exfiltration is causing double-digit million-dollar losses for cyber insurers.

-

Political violence and risk underwriters have heavily cut back in the region, which remains an important source of premium for marine insurers.

-

Reinsurers are also determined to secure structural changes and payback from Italian, Slovenian and Turkish cedants at 1 January 2024.

-

Reinsurers are taking aim at pockets of European risk that escaped retention and rate rises last year.

-

Sources are paying close attention to several pipelines in the region, as the conflict between Israel and Hamas continues.

-

Inflation, supply chain issues and technological failures are complicating the underwriting landscape.

-

Gulf insurers have borne the brunt of reinsurance rate corrections in the past couple of years, but a different, albeit similar market segment is emerging as a focus for concern ahead of this year’s 1 January renewal.

-

The three new capital vehicles fundraising for a Lloyd’s play, coupled with some of the best underwriting conditions seen for years, have raised the prospect of a new age of investment in the market – but questions remain around execution.

-

AI development is creating new risks for insurers to assess as multiple key trends suggest it will evolve into a standalone insurance product like cyber-risk.

-

The business has engaged with the AssuredPartners process, and has also met with a range of other private brokers including Galway and NFP.

-

Insurance Insider has analysed premium growth trends across Lloyd's and the company market for 2022.

-

At an event that brought together construction insurers, brokers, engineers and developers, delegates discussed an impasse over insuring sustainable development projects.

-

Lloyd's has set out what London market firms will need to do to transition from decades-old systems to new central services in July next year, in a crucial step of several modernisation milestones to come in 2024.

-

Despite a return to profitability in marine classes, the market is operating in an increasingly uncertain environment.

-

The worst-case scenario of a $12bn-$15bn claim looks to have been taken out, but there are lots of complex, vexed negotiations still to come.

-

As the curtain comes down on the millionth Monte Carlo Rendez-Vous, and the prices in the cafes and restaurants are presumably reset to their customary levels, the conference has again done its main job.

-

Insurance Insider explores how insurers can manage the dual, polar-opposite pressures of a litigious anti-ESG movement and net-zero climate activism.

-

Industry sources view the letters of credit (LOC) fraud scandal at Vesttoo as a specific rather than systemic failure, with further scrutiny likely on LOC providers.

-

Despite a successful upstreaming of cat risk to primary insurers, reinsurers still have multiple factors to worry about in the run-up to 1 January 2024.

-

An 85% combined ratio and 22% top-line growth are a deserved boost for Lloyd’s – the question is what comes next.

-

A webinar and report from the Geneva Association has explored the barriers and prospects for the growth of blockchain insurance.

-

Key trends the credit agencies will be monitoring include inflation, redistribution of losses and the investment bounce-back.

-

Warehouse or science lab? Those tend to be two of the diverging views on Swiss Re, the oldest reinsurer, with a 160-year history.

-

Hurricane Idalia is still live, but the storm’s track reassured market participants that it will be a relatively minor loss, although one potential wild card is the damage it will cause to Georgia and South Carolina.

-

After Apollo announced a collaboration marking the latest milestone for algorithmic underwriting-led follow capacity in the London market, Insurance Insider explores how such partnerships can proliferate.

-

The story will play out through bankruptcy court filings, but other exposed players and segments will be on watch for ratings agency findings and legal action.

-

Swiss, Munich, Hannover and Scor all delivered optimistic messages on pricing for next year.

-

Ongoing rate rises in property are expected to be offset by decreases in specialty lines and casualty.

-

Most forecasters now predict above-average storm activity for the Atlantic as a result of record-high sea-surface temperatures.

-

London’s major carriers have projected bullish messages on a prolonged hard market for property, while acknowledging other classes are in very different cycles.

-

A fire aboard a car carrier last week raised fresh concerns about the transportation of lithium-ion batteries in electric vehicles.

-

The hammering of hailstorm losses that US homeowners’ carriers reported for H1 will drive positive change in property markets.

-

The first year of data collected in our interactive database of industry people moves is analysed.

-

This publication examined how London market firms are managing post-Covid-19 working practices and found a reluctance to impose mandated office days, but increasing soft pressure to return to the City.

-

New data on the FCA's operational performance shows improvements in some aspects, though response rates are still slow on senior appointment casework.

-

Insurers are messaging that they are able to offset rising reinsurance costs, but will a high-cost tornado season leave them pushing back in the run-up to 2024?

-

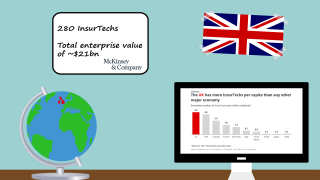

The UK has the highest number of InsurTechs per capita among all major world economies, a new report from McKinsey has found.

-

Fronting companies typically hold premiums in reserve meaning that credit exposure to letters of credit on Vesttoo transactions should only be required in the event of deteriorating losses.

-

Insurance Insider has gathered data on geographical areas prone to cat events, which are outside of southeastern US states, that keep weather experts awake at night.

-

With SRCC losses on the rise in recent years, the French riots have thrown a light once more on the dislocation within the political violence market.

-

Axa’s lack of success in selling its more volatile XL Re segment has led the insurer to cut back on those lines, but the current rate environment makes this a good time to revisit a sale.

-

While Blueprint Two was expected to move the market to a data-first approach, firms have different views on when the industry will reach this new destination and rid itself of document-led processes.

-

The uniqueness of the Probitas business, its management and its backers mean this will not necessarily be a straightforward sale.

-

At this week's Bermuda Climate Summit, speakers heralded the Island's future as a centre of excellence for climate-related innovation and risk transfer.

-

Lloyd's said early adopters could be operating in a fully digital framework by September 2024, with market testing set to accelerate this year with a vanguard group.

-

In the aftermath of an exodus from the NZIA, brokers are concerned that fragmented methodologies adopted by carriers to measure insurance emissions could be a "disaster" for insureds.

-

Three key reports have unearthed issues around capital and lower return period loss figures that may need to be addressed for the cyber market’s maturation, as a pivotal 1 July renewal date approaches.

-

The class is attracting increasing scrutiny from executives and within Lloyd’s, as a descent in pricing persists.

-

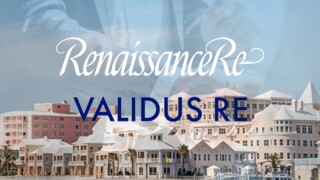

RenaissanceRe has said it hopes to retain as much as 90% of the Validus Re portfolio, but where are the highest areas of overlap by cedant?

-

In this second of a two-part analysis on the proliferation of ChatGPT and similar generative AI tools, Insurance Insider explores the risks inherent in using them.

-

Amid a wide spectrum of views on the proliferation of ChatGPT in insurance, this first of a two-part analysis explores the use cases of automation, data extraction, fraud detection and more.

-

Most forecasters predict below-average activity in the region – but opposing weather phenomena mean uncertainty is higher than usual.

-

Capacity and competition are limiting underwriters’ ability to continue pushing for double-digit rises.

-

The deal is the third scale-up buyout for the firm, highlighting the ongoing value of scale in the reinsurance segment.

-

Early private deals have provided far more stability in this year’s renewal than last.

-

Most carriers were keen to talk about how they are taking on the ongoing hard market in Q1, but some complexities partly offset their good news.

-

Softening cat bond rates are among the bearish signals for cat rates, but latent new demand and still-cautious supply should prolong reinsurer gains.

-

The pace of rate hikes will ease back from the 1 January reset as buyers seek to lock up capacity early after last year’s dislocated renewal.

-

To stay relevant, intermediaries are being forced to scale up, broaden their suite of services and quantify their value.

-

The group’s recent gear shift on growth has elevated the group’s risk profile across areas including M&A, financing, integration and liquidity.

-

The broking group will soon target US retail broking, as well as continuing team lifts and looking for international mega deals.

-

What you need to know about the changes to international accounting standards for insurance contracts, which became effective at 1 January.

-

Lloyd’s has begun to move away from more ‘traditional’ syndicate launches, with a number of recent start-ups aiming to minimise expenses in order to return profits.

-

Shock departures from the Net Zero Insurance Alliance have cast a shadow over the group’s long-term future, as a number of high-profile carriers review developments and consider their ongoing membership.

-

The relationship between consistency and underwriting profitability for Lloyd’s businesses remains steady, our analysis shows.

-

All four quartiles of the Lloyd’s market once again grew GWP in aggregate during 2022, Insurance Insider’s analysis shows.

-

Legal precedents are being set which could lead to crippling liabilities for US businesses as well as longer term data management implications.

-

A higher proportion of syndicates reported year-on-year combined ratio deteriorations than in 2021, analysis shows.

-

Renewals in established markets were more orderly than at 1 January, but smaller markets were under pressure.

-

Five years on from “Project Thunderbolt”, we assess the progress of the start-up challenger broker.

-

Sources said they were seeing more verticalisation of placements in the energy market, particularly in the downstream segment.

-

London D&F underwriters are seeing rate rises of 20% on average amid surging in-flows of new US business ahead of the key 1 April renewals.

-

Last week’s headline results were in line with preliminary figures, but here are three Lloyd’s stories you may have missed.

-

In the aftermath of Silicon Valley Bank’s 11th-hour rescue, InsurTech investors have ramped up systemic risk controls across their portfolios amid a tightening funding landscape

-

This publication’s tally of disclosed insured losses resulting from Russia’s invasion has increased 18% to $3.1bn.

-

The demise of the lender underlines concerns about global economic conditions and high interest rates.

-

The combined ratio reported by Lloyd’s for 2022 would put it in the top half of Insurance Insider’s peer group, analysis of preliminary results shows.

-

Lloyd’s has drawn attention to an improved attritional loss ratio in 2022, warning the market that it would be “very difficult to get back” if it slips.

-

The release of Swiss Re, Munich Re, Hannover Re and Scor’s year-end reports provides an update on market conditions.

-

With brokers shifting to new providers to place certain classes, and competition among e-trading firms intensifying, the placement platform landscape has reached a crucial turning point.

-

Beazley executives spoke of further growth prospects in the class, after its results revealed a 79% combined ratio for its cyber division in 2022.

-

At the InsurTech Insights Europe event last week, experts explored how AI is on the brink of being commoditised in underwriting.

-

A canvass of Lloyd’s market executives generated an expected combined ratio of 92%-93% for 2022.

-

Two of the most-exposed segments to the war have experienced very different years, with sweeping PV changes contrasting to more stable conditions in parts of the aviation sector.

-

The conflict is set to inflict billions of dollars of losses across the specialty insurance market.

-

Topics discussed included Caribbean cat risk, protests in Peru, crisis in Argentina and the World Cup.

-

There has been no let-up in rate reductions so far this year, as fears mount about the profitability of the class.

-

Slowing primary pricing, the looming threat of inflation and increased cat retentions were key themes from this reporting round.

-

Marine and aviation markets among most active parts of the industry in recent months, data shows.

-

Cyber rates in excess layers saw decreases of mid-single digits to low double digits in the last quarter while primary layers remained flat or experienced low rate rises.

-

Early evidence is leading the (re)insurance market to hope the storm can avoid the development curve of its 2017 predecessor Hurricane Irma.

-

Annual reviews of natural disaster activity highlighted drought – which can also heighten risk of fire and flood losses – as an increasingly important secondary peril.

-

Carriers will be looking forward to the positive outcomes from the 1 January harder market, but results will provide clarity on lingering challenges.

-

More quota share capacity was on offer, but reinsurers were still pushing to manage exposures through loss caps.

-

Insurers are looking to buy fac protection to cope with increased retentions on treaty programmes, while exclusions around political violence could also boost demand.

-

At least $7.8bn in reserves was transferred from the live market to legacy carriers last year, with Enstar the leading acquirer.

-

Despite a cooling economy, cost of living pressures are keeping wage inflation and mid-pay employee pressures on base.

-

Specialty reinsurers clamped down on Ukraine coverage at 1.1, with the one-year anniversary of the invasion threatening claims.

-

Here we walk through seven themes of the market that will be drivers of change in the year ahead.

-

Cedants are grappling with rising rates while coverage narrows.

-

Cedants who came to market in Q4 settled for smaller tranche sizes in recognition of limited capacity.

-

Reinsurers have successfully pushed hard on T&Cs but, as capacity begins to fall into place, there are still many unanswered questions for this renewal.

-

The major trends and developments of the last 12 months in (re)insurance, in charts.

-

The London market proved resilient in the face of twin shocks from geopolitical and natural disaster.

-

The European cat market is hardening faster than expected but the process is being delayed by ongoing negotiations over retro protection and varying lists of reinsurer demands to improve terms.

-

Carriers and brokers in particular will start to change key processes next year as the market adopts foundational elements of the Blueprint Two programme.

-

In a review of financial services firms’ D&I policies that highlighted shortcomings, the regulator said policies need to be holistic, and not generic.

-

Specialty reinsurance is facing a similarly fraught and last-minute renewal as that seen in property cat.

-

After an annual update from Lloyd’s CEO John Neal on the progress of Blueprint Two, Insurance Insider delves into the delays and what was actually delivered.

-

In last year’s survey, only second-quartile syndicates reported aggregate year-on-year growth of more than 10%.

-

The risk is increasing of some cedants ‘running naked’ in early January as the market faces a ‘horrendous bottleneck’ of negotiation ahead.

-

The increasing frequency of $1bn-plus deals has led to discussion in legacy circles on whether there is a viable case for legacy deal syndication.

-

Eight syndicates including newer vehicles from CFC and others, as well as mature vehicles from Everest Re and Lancashire, have so far reported increases in stamp capacity of 50% or more.

-

Panellists at the London Market Conference called on the industry to work together to improve recruitment, the experience of staff, and its own image.

-

Initial loss estimates for the last quarter show lower hits to equity than observed after hurricanes Harvey, Irma and Maria five years ago.

-

The French reinsurer’s Q3 update details its extensive remedial efforts – but with the impact yet to be felt, it is still vulnerable to takeover.

-

The aviation market took what is believed to be its largest-ever loss recently and court actions over Ukraine claims are ongoing, all contributing to a hard war market as all-risk renewals remain softer.

-

Some multi-national cedants are using US addresses to source cover from US carriers, risking issues in the event of claims, amid a desperation for growth on both sides of the Atlantic.

-

The hurricane could prove a key test of the London market’s efforts to reduce catastrophe exposure, but will local carriers be able to lean into the hardening market?

-

Inflation, heightened cat activity and years of poor reinsurance returns are fuelling demands for wholesale change in the European market.

-

Many policyholders are likely to receive larger payouts following the judgement, but a worst-case scenario has been averted.

-

Cedants may find past behaviour coming back to haunt them, while brokers should be preparing in depth to achieve simplicity.

-

Reinsurers are demanding price increases and higher retentions as brokers warn cedants to be ‘realistic’.

-

Plus the latest executive moves and all the top stories of the week.

-

In a canvass of London market professionals, most placed their “gut feel” industry loss estimate for Hurricane Ian at $40bn-$50bn.

-

With significantly lower retentions, AIG, Assurant and Allstate are more likely to pass the cost of the hurricane onward to their reinsurers.

-

The latest statistics from the IUA show that the Lloyd’s market perhaps has not conceded as much ground as initially thought.

-

Sister title Trading Risk ran some scenarios applying market share figures and loss ranges to paint a picture of how the quantum of trapped capital could evolve.

-

In 2022, the NFIP placed reinsurance with 28 private companies - including 13 Lloyd’s syndicates.

-

As it became clearer that the Fort Myers area was facing 150 mph winds, sources started to talk about loss estimates with a $30bn floor.

-

Research by sister title Inside P&C shows the top three homeowners carrier exposures by county for forecast highest impact areas.

-

Inflation and reinsurance costs are among the key challenges that marine underwriters face.

-

Cat 4 Hurricane Charley made landfall on Florida’s west coast in 2004, while Tarpon Springs (1921) was the last major storm to hit Tampa.

-

Reinsurers are better positioned to face this storm from a financial point of view – to Florida state’s detriment – but how capital providers will react to a loss is the wildcard.

-

Inflation will define priorities such as a focus on safeguarding clauses and pricing transparency, as well as line of business challenges, for underwriters and actuaries in the year ahead.

-

This publication’s review of H1 disclosures shows how listed (re)insurers’ nat cat losses have tallied with aggregate projections.

-

Sources said that some entities were exhibiting “sheer desperation” to hit 2022 plans, driving down prices.

-

How much capacity is available to meet rising cat reinsurance demands was a key theme throughout this year’s Rendez-Vous.

-

Political violence reinsurance capacity will be a “precious commodity” at 1.1 but differences remain over how much restructuring of specialty composites should occur.

-

Negotiations may focus on attachment points and the extent of double-loading for inflation.

-

The H1 story has overall been a positive one for Lloyd’s, but the market and the Corporation are entering a period which will be characterised by huge uncertainty and volatility.

-

Data shows that last September there was an uptick in commuter activity in the City, but a repeat in 2022 is uncertain.

-

Yesterday, we published a detailed examination of the barriers preventing women from reaching the executive committees of Lloyd’s managing agencies.

-

In the first part of a two-piece investigation, Insurance Insider explores the pernicious barriers to women reaching the executive committees of Lloyd’s managing agencies.

-

The Corporation has resequenced a key Blueprint workstream for delegated authority business, as it looks to create a data strategy for DA in Q4.

-

The Ukraine loss reserve tally has reached $2.4bn as of the end of June.

-

Odyssey Group’s cyber chief Robert O’Connell is looking to raise up to $1bn of capital for a monoline cyber reinsurer.

-

Swiss Re, Munich Re, Hannover Re and Scor have set out their strategies on inflation, pricing and Ukraine.

-

The first six months have been characterised by substantial double-digit growth and further improvement in underwriting performance.

-

The carrier reported a H1 combined ratio of 74%, as it targets $1.3bn in cyber premium for the year.

-

(Re)insurers have used Q2 reports to reassure investors of their proactive approach to inflation – and stress some of the longer-term benefits.

-

The Hong Kong-based carrier and its backer have been placed on negative review by the ratings agency, prompting questions around its future.

-

Carriers in the class are reassessing risk appetites amid inflation, the Ukraine war and a growing risk of countries defaulting on sovereign debt.

-

North American companies also pay executives more relative to company size than European rivals.

-

The median 2021 compensation of industry leaders in the US and Canada was $7.7mn, compared to $4.9mn in Europe.

-

Inflationary pressure, increased demand and negotiations over attachment points are among the factors that reinsurers believe are ramping up pressure in the catastrophe space.

-

Metromile’s Preston and Lemonade co-CEOs Wininger and Schreiber all joined industry stalwarts in this year’s top 10.

-

Claims inflation and the risk of a major marine war loss crystalising in March 2023 is looming over an otherwise buoyant marine market.

-

Following the war in Ukraine, sources expect an uptick in reinsurance costs, a decline in risk appetite and business moved away from market facilities.

-

Are we set for the shortest softening D&O market ever?

-

As London market carriers encourage parental leave take-up, Insurance Insider explores whether the HR benefit can be a tool to tackle the industry’s diversity issue.

-

The French reinsurer faces a number of hurdles as it looks to set its new corporate strategy. We outline the challenges ahead.

-

Organisers perceive a clear runway ahead for planning events, after over two years of restrictions on gatherings.

-

Insureds are also buying less limit to manage spend, which is impacting the flow of business to the London excess market.

-

While aggregate premiums grew by 1.5x between 2012 and 2021, annual expenditure at Lloyd’s on salaries and other employment costs has doubled.

-

Sources in the market estimated the average risk-adjusted rate increase at the 1 June renewal at around 5%, with a similar trajectory expected for 1 July accounts.

-

Competition for business is leading to a rollback in exclusions written into contracts following major loss activity.

-

The forecast range of hurricanes is slightly wider than in 2021, but in line with 2020.

-

As momentum builds for greater transparency on ESG and net-zero transitions across the insurance ecosystem, brokers are entering an evolution.

-

Sources close to the industry are calling for litigation reform as a priority, while Florida Hurricane Catastrophe Fund expansion is also on the cards.

-

Ukraine uncertainties remain despite some loss estimates emerging in Q1 earnings across the Big Four European carriers, while inflation looms on the horizon.

-

Recent start-ups have recorded annual underwriting losses about 80% of the time, Insurance Insider analysis shows – even after becoming established.

-

It is understood that the Marsh and Aon Alpha facilities are those with the most exposure to the war in the Ukraine.

-

Swiss Re goes against the tide in expanding in cat, while specialty rates appear to be holding up better than expected.

-

A second setback to the delivery of PPL’s Next Gen’s platform has triggered questions among firms about confidence in any new timeline.

-

Rates are experiencing a slow taper but eventual Ukraine claims figures are difficult to gauge.

-

The possibility for lessors to claim on airline policies has added another layer of complexity to the unprecedented loss scenario for aviation.

-

The most profitable syndicates tend to be consistent performers long term, Insurance Insider analysis shows.

-

With the Lloyd’s Lab in its fourth year and poised to welcome cohort eight to its incubator, Insurance Insider examines its impact so far.

-

Only the top quartile increased GWP between 2019 and 2020.

-

Only 31% of syndicates reported underwriting losses in 2021 – down from 64% in 2020.

-

The escalation of conflict in Ukraine has led to global energy uncertainty and underpinned high asset prices.

-

Lloyd’s improved its underwriting performance relative to its most directly comparable peers in 2021, Insurance Insider analysis shows.

-

There is a tension between securing payback and negotiating higher retentions.

-

Management commentary and disclosure from the Lloyd's 2021 result outlines key challenges for the market ahead.

-

The second of Insurance Insider’s deep-dive analysis pieces on innovation examines the internal structures and opportunities that can accelerate innovation.

-

The first of a two-part series on innovation examines the barriers blocking product innovation in the P&C market.

-

The theme of yesterday’s market briefing is that Lloyd’s is now moving into a period of growth, having completed remediation, but it wants smarter, sustainable growth.

-

Growth plans are common in the market but there are questions about the level of rating adequacy.

-

Earnings reports from Swiss Re, Munich Re and Scor have revealed increased cat budgets and highlighted continued shifts away from frequency coverage.

-

Insurance Insider does the data work on how Ki’s first-year numbers compare with other Lloyd’s start-ups.

-

Underwriters are navigating tricky territory as they look to hit growth targets while maintaining discipline on pricing.

-

Improved underwriting performance and double-digit top line growth at most carriers has characterised results reported so far.

-

Scor’s renewals update denotes a continued push to control volatility while Hannover Re is focused on growth.

-

A hardening market, competition from start-ups and macro conditions have combined to drive up staff costs.

-

With government guidance lifted, there is a growing pressure for an in-person presence in the London market.

-

London market intermediaries are benefiting from rocketing organic growth and boosted revenues.

-

Data obtained from PRA and FCA shows fewer Skilled Persons Reviews in recent years – but the tool remains a valuable one for regulators.

-

Increased competition is shifting market dynamics after a transformation in rating conditions.

-

Fire season in the US ran slightly later than usual in 2021, but total losses will fall far short of 2017-18 peaks.

-

The catastrophe market, inflation and loss-costs and the pandemic unwind are among the trends to shape the news agenda this year.

-

Property cat rate increases this January were double those of last year and the highest since 2014.

-

The insurance industry will hope to maintain rating resolve and withstand the forces of inflation in 2022.

-

New capital made its presence felt in the market in a year that saw both the completion and collapse of major business combinations.

-

The market was divided about the outlook for 2022, with some predicting a substantial reduction in rates.

-

The major marine classes have undergone substantial remediation, which has attracted new capital to the space.

-

All quartiles of the market are expected to increase aggregate stamp next year, analysis shows.

-

Autonomous shipping and complex supply chains make the maritime industry vulnerable to cyber disruption.

-

Amid an onslaught of announcements on climate disclosure requirements, listed insurers have a limited timeframe to prepare.

-

The market is assessing whether planned single-digit rate rises will outstrip burgeoning claims inflation.

-

Swiss Re, Munich Re, Hannover Re and Scor have set out divergent strategies on cat as volatility increases and the retro market seizes up.

-

Aggregate reported net losses from Q3 catastrophes across the (re)insurance industry have now passed the $20bn mark, analysis by Insurance Insider shows.

-

Sources say the insurance industry will not walk away en masse from existing clients.

-

Male board members still hold more than two thirds of all seats at listed carriers and brokers, analysis shows.

-

Data published by the NOAA illustrates a low incidence of hurricanes later than October over last 30 years.

-

Review of quarterly financial updates released so far shows Bermudian carriers wearing major losses.

-

Cedants prepare for market-wide increases despite lack of clarity post-Baden Baden.

-

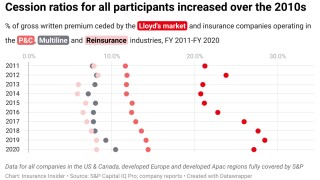

Analysis of financial data shows that the last decade has seen a marked increase in the proportion of premiums ceded by carriers in all sectors.

-

Amid three regulatory consultations for the legacy market and the threat of s166 reviews for certain Part VII transfers, the legacy market is reaching a turning point.

-

Increased disclosures being released by companies heighten the risk of inaccurate or misleading statements.

-

How well has Howden future-proofed itself against key issues around the group’s culture, shape, ownership and succession plan?

-

Claims from recalls due to lithium-ion batteries, which are heavily linked to the sustainable auto industry, are causing a capacity squeeze and affecting rates on certain policy lines.

-

The carriers with the largest Louisiana market shares also ceded more than $100mn to Lloyd’s syndicates during 2020.

-

The Financial Conduct Authority’s latest release on UK claims data for Covid-related BI losses shows the total number of claims is starting to stabilise.

-

An increase in participants in the class of business could risk derailing underwriting remediation efforts.

-

While some Lloyd’s stakeholders are frustrated by the lack of visibility on Blueprint Two reforms, the Corporation is poised to up the ante on engagement on timeframes.

-

Most survey respondents want to travel no more than once every two months for work.

-

Insurers said it’s too early to talk loss quantum, but believe they are well poised to deal with any future losses.

-

Despite a somewhat mixed outlook, UK listed carriers London players say they are still leaning into growth.

-

The number two broker must now refocus on rebuilding internal divisions.

-

With a last-minute acquisition by AJ Gallagher on the cards, Willis Re can put the last 16 months of turbulence behind it and come back super-charged.

-

Reinsurers using Europe primarily as a diversifier to counter risk in peak cat zones are increasingly faced with significant loss events on the continent.

-

Many market participants have managed to curtail their admin expense ratio over the last five years, although correlation between GWP and cost-efficiency remains weak.

-

Willis Towers Watson must act quickly and decisively to either salvage the sale of Willis Re or lock down staff.

-

Huge disputes over aggregation of claims and ongoing coverage disputes point to uncertain overall exposures.

-

Some observers questioned whether Hiscox would have benefitted from the bigger shake-up of an external hire.

-

Analysts believe 2021 will be a “transition year” for Hiscox, Beazley and Lancashire.

-

Underwriters warned of a need to sustain profits and the risk of losses as plants are reactivated.

-

The Financial Conduct Authority’s latest release on UK claims data for Covid-related BI losses shows an acceleration of acceptances during June.

-

Over the past decade, the high degree of fragmentation within the UK retail broking market has attracted private equity investors intent on consolidating intermediaries to create additional value.

-

There has been an uptick of event cancellation business flowing from the US, which is attracting rate rises of around 50%.

-

Reinsurers are talking about a new era of elevated risks, but their behaviour may signal a more relaxed view heading into 2022.

-

US property rate increases are coming in below expectations, although European rates remain on the up.

-

The Corporation’s deal signals a moderate view on growth and a refined approach to solvency management.

-

New entrants have eased the capacity constraints that played a large part in last year’s huge rating changes.

-

Senior executives on the island saw the coordinated initiative as a clear long-term threat, but one that is mitigated by various other attractions of operating in Bermuda.

-

The London market has seen a marked slowdown in specialty insurance rates year-on-year, in the latest evidence that the recent upswing in rates is starting to lose steam after three years of acceleration.

-

State-backed carrier GIC Re faces competition as the European Big Four press into the subcontinent.

-

On average, syndicates which show consistency in their underwriting results also deliver higher underwriting margins.

-

The results challenge the idea that syndicates need to build scale at Lloyd’s in order to succeed in the marketplace.

-

Whatever their eventual impact on runaway loss inflation the fact reforms were enacted at all is a happy surprise for the industry.

-

Many carriers agreed on the growing attraction of primary markets but differed on reinsurance-expansion tactics.

-

The February Deep Freeze has already pushed cedants to access reinsurance, adding fuel for rate rises later this year.

-

Analysis of the numbers by Insurance Insider showed a slight loosening of the Corporation’s restrictions on growth between 2019 and 2020.

-

Underwriters voiced a cautious optimism about the outlook for 2020, but warned that the class was moving from a low point.

-

After years of poor performance and talent flight, Insurance Insider examines the challenges faced by Axa XL and the strengths it holds to forge a new start.

-

An increased frequency and severity of fires weigh on per-risk covers.

-

Willis Re data on Florida participants’ deteriorating CoRs and solvency highlights the challenges to be faced at this year’s 1 June renewal.

-

Hannover Re has emerged as an outlier by reducing its overall 2020 dividend, but its growth plans may alleviate disappointment about the policy.

-

As some in the market believe the winter claims will remain notably below $20bn, there are multiple factors creating challenges in assessing the event.

-

We assess the hurdles facing the marquee specialty insurance franchise, including staff retention and the fallout from the UK BI saga.

-

The fourth quarter, while down on Q3 and a year earlier, was the sixth-highest three-month period since tracking began in 2010.

-

Market sources said that ongoing economic disruption is likely to keep pricing in the market high.

-

The majority of London underwriters said they expected rates across their cyber book would be up 30% for the year.

-

Disclosure from the firm’s cyber and executive risks division shows a rapidly hardening market with a fast-evolving claims profile.

-

Further Covid losses, core loss ratio improvements, reserving and the duration of the cycle are key themes emerging from the reporting season.

-

Fenchurch Law partner suggests "aggressive" initial claims adjustments will be unwound and the reinsurance context will need specific consideration.

-

Conditions remain favourable for underwriters but uncertainty remains on whether the recession will lead to a flood of claims.

-

Economic headwinds combine with high valuations to create greater impetus for intermediary sales.

-

This publication looks at 10 issues that will shape the industry in the year ahead, from rate sustainability to start-up progress to the post-Covid recovery.

-

The AJ Gallagher report says multiple potential claims could take current loss levels well above the $330mn already known about.

-

Nearly 75% of StarStone International senior underwriting staff are now in new roles.

-

Retro rates are at an eight-year high, according to the broker.

-

The broker’s 1st View report said rate change may have disappointed some reinsurers but remediation focused on specific stressed pockets of business.

-

US cat renewals are outpacing European increases, but as signalled earlier this month, the level of rate hikes has fallen back.

-

There will be significant movements in the ranks of the top 10 syndicates in 2021, with Brit moving into second place and Axa XL tumbling to 7th.

-

Further analysis of our annual survey reveals the biggest movers in the market and the combined impact of new entrants for 2021.

-

A full breakdown of stamp capacity movements for 2021 from this publication’s annual survey.

-

The client tool will provide real-time data on pricing, profits and claims.

-

The capital skewed to scale-ups, London and carriers targeting both primary and reinsurance business.

-

Cedants and reinsurers perform a "slow dance" around pandemic losses, with claims negotiations deferred beyond renewal.