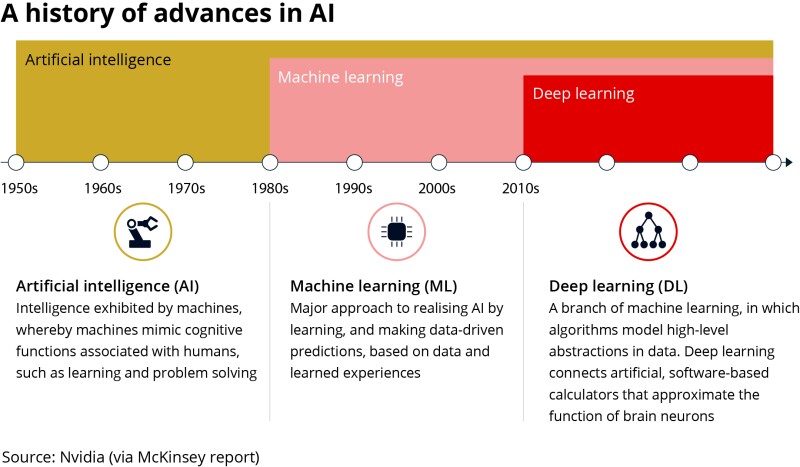

Generative AI (GenAI) has been described as “the next internet”, an advancement in technology that will fundamentally change the way we work.

As insurance market participants have started to explore ways to invest in GenAI over the past year, the immediate starting point has been “low-hanging fruit” applications of the technology, which can provide support straight out of the box.

But looking to the future of AI, sources outlined how the introduction of the technology may well bring about significant changes, such as increased regulation and a shifting workforce.

Last year, former deputy editor Marcel Le Gouais laid out the opportunities and risks of GenAI, particularly ChatGPT, for the industry.

Now, a year on, this potential has already become more practical with the technology being implemented by companies across the industry.

This analysis which will delve deeper into precisely how GenAI is and will continue to change, help, and hinder the insurance industry. First, we will investigate how GenAI is already being used throughout the industry, and then consider the GenAI of the future.

Low hanging fruit

When discussing how GenAI is already being used in the industry, sources repeatedly described several “low hanging fruit” early uses, which some firms could employ and see benefit from almost immediately.

They referred to the simple, out-of-the-box and internal uses which have a much lower risk of violating General Data Protection Regulation (GDPR), or regulatory controls.

First, sources explained that AI could help to solve a longstanding data problem in the market of relying on unstructured data that often needs re-keying when being shared.

It is possible to use GenAI to extricate data from a word or PDF, exporting the data into a format that makes it useful to the carrier or broker.

But sources warned it should not be mistaken as a quick fix for a company's poorly structured and organised data.

Farris Salah, head of smart-follow at Apollo, said that before a company invests too heavily in AI, it should first invest in digitising data, integrating systems, and automating processes, explaining “it’s easy to hope in shiny objects but it’s better to believe in solid foundations".

For companies that have invested in cleaning and organising their data, and which are ready to start picking up the ‘shiny objects,’ sources believe the next area to focus on is an in-house chat bot, which have been in use for years in frontline customer service. These are already being employed by companies such as Moody's RMS, and Zurich.

Sources explained that internal chatbots can be useful for making organisational knowledge, compliance information, and company documents quickly accessible, rather than requiring staff to manually interrogate a wealth of documentation.

By using GenAI to take existing processes within the industry, and combine it with technology, staff are freed up to be "a lot more productive," sources explained.

Other uses of the internal chatbot are for claims handling and customer service.

By quickly being able to interrogate a client’s policy, answers to questions can be given in a timelier and (hopefully) accurate way, leading to happier customers and a better service.

Part of the reason that the above uses are considered the 'low hanging fruit', is because for an insurer or broker looking to invest in GenAI, most of the above use cases can be implemented close to out-of-the-box.

Further, because these cases do not require the collection of external data from customers, and do not make decisions based on customer data, the uses are not strictly regimented by regulators.

A source explained that these examples show where you can plug in a product like AI into an insurance company and "create efficiencies without screamingly obvious regulatory risks coming up", because you are not using a person's details and you do not necessarily have to deploy it into a sensitive type of product.

Future uses and underwriting fears

Generative AI (GenAI) is set to change the way the world works, and may cause significant changes throughout the insurance industry, including changing the profile of the workforce as carriers consider how to integrate it more deeply into underwriting operations.

Personalisation

Sources canvassed explained that alongside the more immediate uses as laid out in Part 1, GenAI can be used to bring a level of personalisation to insurance that is yet unseen.

“AI can make [underwriting] more sophisticated and more personalised,” said Eddie Longworth, director, JEL Consulting, and founder of the Code of Conduct for the Use of AI in Claims.

A source explained that with the high volume of data and the use of GenAI, you can start to break down a pool of risk into segments and micro-segments because you are able, with so much data, to underwrite on a very precise basis.

However, sources have warned that hyper-personalisation, which would be very easy with GenAI, could fundamentally go against the insurance model of diversifying risk.

One legal source questioned: "To what degree can you promote granular underwriting? Because if you keep on reducing the size of the pool by personalising more, then you end up with smaller and smaller pools, which means that your premium will become more volatile".

They added that the use of GenAI to help personalise and thus bring down the cost of products is great, but “that the data has to be in exchange for better pricing”.

What regulators do not want to see, they explained, is a worsening effect on people in which they have to provide data to get products. Regulators do not want it to become a requirement for people to have to hand over their data and to stop smoking for example, to obtain coverage.

That will be particularly acute in retail lines such as health and life insurance, they added.

Enhanced underwriting

Beyond the low hanging fruit, the sector is also looking towards “automated underwriting” to free human underwriters from more menial tasks.

Sources told this publication that although it is not likely to replace underwriters any time soon, GenAI can help carriers perform “underwriting better”.

One source believed GenAI could assist portfolio management: "The AI is able to look at a book of business and assess if are they overexposed to a particular risk, for example."

By introducing GenAI to help with that part of the underwriting decision making, as well as the pricing process, sources said that carriers can “take the onus off what could be an imperfect or incomplete human memory” or fill a gap if someone is on a holiday.

Some sources argued that underwriting is often already completed by a machine, with human input. Longworth added that GenAI "can make that more sophisticated and more personalised".

Further, Leon Gauhman, chief strategy officer at digital product consultancy Elsewhen, explained that in the short term, “there's [a] huge amount of value that can be unlocked by just making the underwriters’ work simpler”.

He explained that this includes being able to take information from a format that currently takes a lot of time to collect and understand, such as organisational expertise or knowledge of compliance standards and processes, and present it in a format that is accessible for immediate use.

However, companies looking to invest in GenAI must do so with a clear understanding of the problem they are trying to solve, rather than just jumping on board the GenAI trend, a source warned.

AI as an underwriter

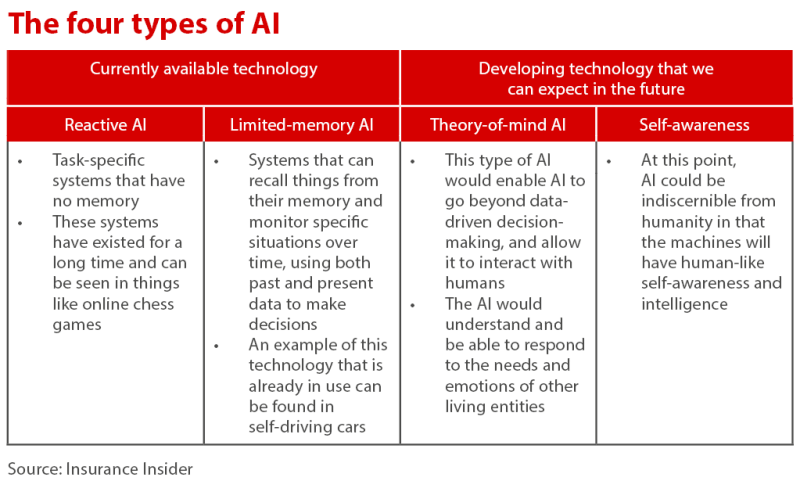

Sources did not agree on whether it would be possible for GenAI to take on the role of a lead underwriter.

One source suggested that GenAI will eventually be like an Excel spreadsheet – a tool that underwriters employ, as opposed to it taking over the underwriter’s role completely.

Uniqueness is the villain to AI

Some argued that in the case that GenAI would take on the underwriting role, it would be best suited to the simpler task of providing follow form capacity, rather than replacing lead underwriters in the London market.

As an additional challenge, London market leaders typically have to deal with complex risks that cannot be written as easily elsewhere. As one source noted: “Uniqueness is the villain to AI.”

Another source said that they simply do not believe that regulators would allow GenAI to take on the role of a lead underwriter.

Others, such as Longworth, argued that GenAI could be a lead underwriter in areas of less complex risk and GenAI could help underwriters understand those much more complicated risks.

A new workforce

Assuming that GenAI is unlikely to “take over” from lead underwriters in the London market may raise the question, however, of what the future workforce may look like for the GenAI generation.

“We are a long way from AI replacing underwriters. As soon as you remove people from the loop, there are a lot of ethical questions that we are not even close to being able to answer or think through. Going forward, GenAI systems are going to be designed in a way that still allows people to make key decisions,” Gauhman said.

“I don't see any future that is going to be completely dehumanised,” he added.

Many sources agreed however, that the workforce would change as humans and GenAI work together.

This change in profile would include more staff focussed on training and working alongside GenAI, but all sources agreed that the new technology will not be taking over traditionally human roles any time soon.

I don't see any future that is going to be completely dehumanised

One concern that has been expressed several times in conversations regarding GenAI is that it will take over data entry and entry level jobs, because many trainees end up doing those repetitive tasks which AI is so well suited for.

The concern, then, is what happens when the industry finds itself struggling for talent, because AI has taken the entry level roles.

However, more sources believed that this could open ways to create better entry level roles, with more suitable and effective training.

One source noted that this is not a GenAI issue, so much as an industry one. “If you think sitting at a box doing data entry is a training programme, you should go and walk out the door.”

They added that a new starter to the industry would “learn almost nothing other than the data scrap knowledge, as opposed to when you make decisions.”

Salah said that many areas of AI, including Gen AI, should significantly free up time for underwriters, and create new and exciting opportunities across insurance, attracting exceptional talent into the industry.

"There is an unfounded fear that AI is coming for people’s jobs. I believe it will be a catalyst for a thriving culture, built on an environment that enables more human interaction, rewards curiosity, and facilitates productivity. I am very positive on the future."