Analysis

What is causing the tensions building across the insurance market in 2026? A softening market is breaking apart the coalition of aligned interests that the hard market held together, and structural changes built up since 2017 are making those strains worse. This analysis shows how the pressure is fracturing along three main lines: retail against wholesale brokers as they fight over a much larger E&S commission pool, insurers against the MGAs, fronts and facilities they backed in the hard market, and investors against management and staff as returns compress. It delivers fast insight on which of these fights are simply cyclical and will ease when rates turn, and which expose deeper structural cracks that will keep cannibalising carrier value even in a rising market.

Subscribe to get comprehensive access to our exclusive analysis in the full platform.

Mounting soft market tensions are breaking the broad hard market coalition.

In March, levered broker Patriot Growth suddenly parted ways with its founding CEO Matt Gardner.

As value creation slowed in an unsupportive market, it is understood that Gardner clashed with lead investor GI Partners around the value creation plan. That clash precipitated his exit.

Patriot is just one highly visible example of the way the mood music of the market is changing in 2026.

The hard market built a coalition of more-or-less aligned interests, creating conditions in which every intra-company stakeholder group and every participant in the value chain could win.

Soft markets inject stress.

That stress is now fracturing the hard-market coalition, and sowing rancor in the market.

Some of this is always to be expected at this point in the cycle. But structural changes in the market, including the growth of the big wholesalers, the deconstruction of the underwriting value chain and increased PE-backing of retail brokers, are aggravating the typical cyclical tensions.

Those changes, in addition to the E&S wave, the secular shift to MGAs, the rise of the fronts and the massive proliferation of levered PE-backed brokers, have recalibrated the industry structure. The structure – largely assembled since 2017 – is now being tested by its first soft market.

Fracture 1: Retail vs wholesale

Retail brokers are fighting with wholesale brokers across a range of fronts.

The retailers have all been going through rationalization exercises, pushing the wholesalers to compete against each other for coveted panel positions and re-cutting commission arrangements as they do so.

This is flowing downstream to E&S insurers, with commissions on wholesale business often moving up from 17.5% to 18.5%.

There is also a push from retailers with wholesale operations like AJ Gallagher and Acrisure to redirect business from third-party wholesalers through their own wholesale arms.

Elsewhere, retailers are simply looking to place the business direct without using the wholesalers at all, insourcing placement.

Alongside this, retail brokers are exerting some soft pressure on dual-channel insurers not to take business from the wholesalers.

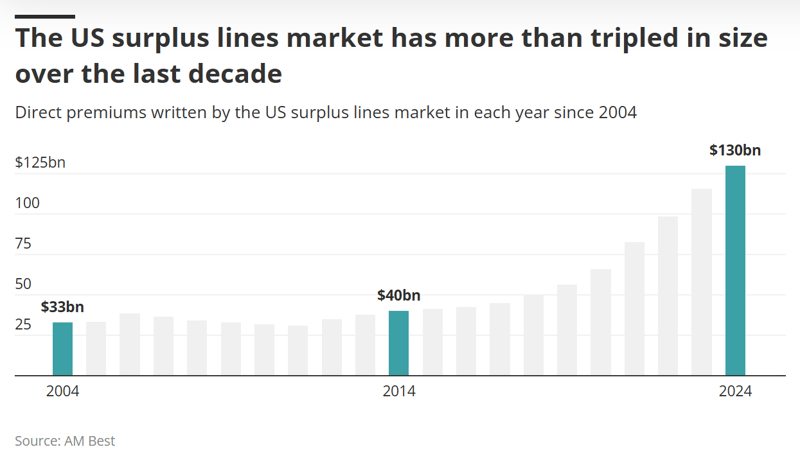

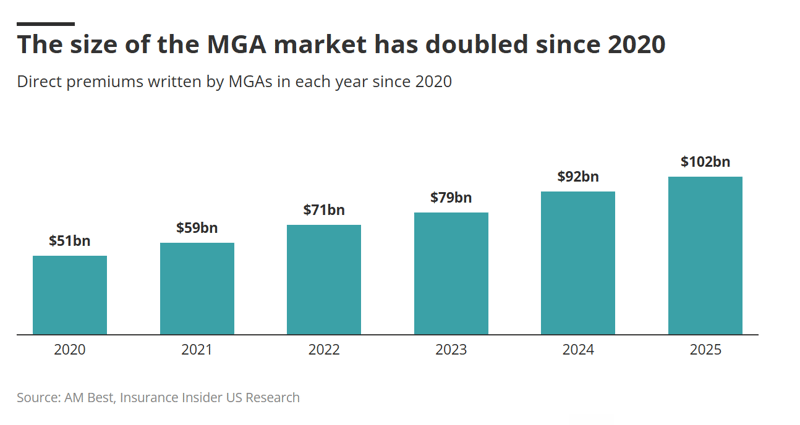

Commission fights are nothing new, but the E&S market has grown from less than $50bn of premiums in 2017 when the last soft market ended to $130bn in 2025. Far more is at stake this time.

Fracture 2: Insurers vs MGAs/fronts/facilities

Insurers, meanwhile, are pointing fingers at the deconstructed underwriting value chain as an accelerant of the soft market.

In a hardening market, (re)insurers were happy to throw their capacity behind MGAs, fronting companies and (in London) broker facilities.

But, as the market comes off, agency problems are starting to emerge as MGAs and fronts chase growth to drive Ebitda higher as a means of creating equity value, while carriers brace for deteriorating underwriting results.

These pressures are amplified by the overextended value chain, with greater distance between the underwriting decision and the end capital than in previous cycles. The MGA market has also just taken massive share from direct writers since the last soft market.

As frustration with this ecosystem grows, insurers providing major support to broker facilities are also catching flak from their rivals for throwing fuel on the soft market fire.

Allianz’s foray into E&S by supporting CRC’s new 30% cross-class capacity deal has come in for criticism, as has AIG’s 25% follow-form facility deal with McGill and Partners.

Sources have said that these kinds of deals give distribution too much power at the wrong moment.

The irony with (re)insurers attacking the deconstructed underwriting value chain is that they are providing the capacity that allows it to run.

Fracture 3: Investors vs management vs staff

Brokers are suffering from slowing organic growth, which is compressing returns that had already been crimped by the increased cost of debt and reduced merger arbitrage.

Patriot’s CEO change is the most extreme example, but across the brokerage segment, the deteriorating return profile is fraying the stakeholder coalition between investors, management and staff.

In private companies, the pressure could manifest in trade sales in the face of management opposition, swingeing cost-cutting programs or deals at valuations below the face value of staff common equity holders.

The interests of investors, management teams and staff are diverging. Acrisure’s 11% headcount reduction program last month was a clear illustration of this and a sign of things to come.

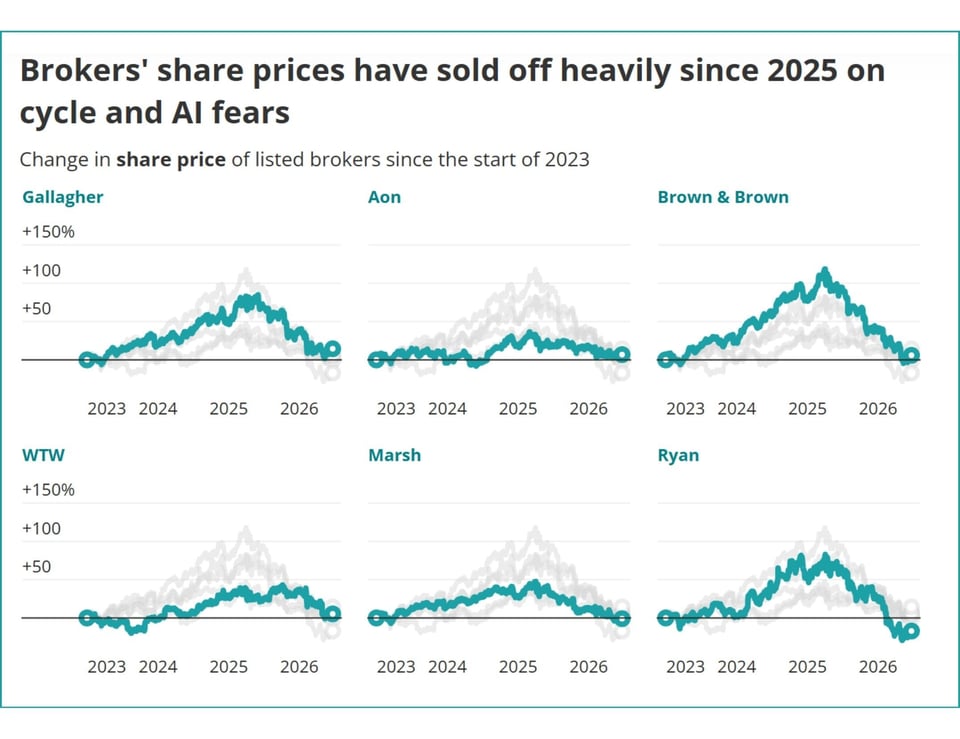

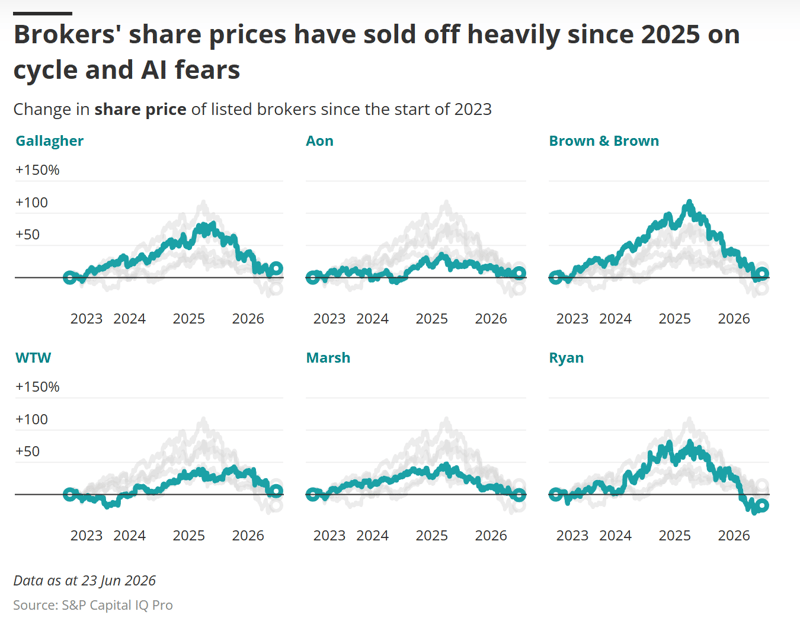

Public brokers are facing their own version of these internal tensions, with pressure dialing up a two-stage sell-off driven by the P&C cycle and AI disruption fears.

The worst-affected brokers, Ryan Specialty and Brown & Brown, are down close to 50% over the last 12 months.

As a result, staff incentive compensation is underwater – hurting staff that have grown used to easy wins.

With investor scrutiny intense, management teams are not rebasing the compensation. To make matters worse, some are cutting bonus pools as they strain to show margin improvement to investors as organic growth slows.

This is only going to fuel the increasing prevalence of team lifts.

The practice has become increasingly widespread as it has become clear that the courts provide insufficient protection to incumbents.

Still, the courtroom fights and the commercial retaliation seen against the Howden US build-out are further adding to the fractiousness in the sector.

Tension wherever you look

These are some of the crucial flashpoints, and they reflect the structural changes in the sector over the last decade.

But everywhere you look, there is tension.

Insurers and reinsurance brokers are blaming reinsurers for the indiscipline of 20% rate cuts on cat, grousing that it will accelerate property insurance softening and douse broker organic growth.

Insurers are resentful about a commission drive from brokers that spans base brokerage, panel fees and the hard-sell on data products that they don’t want.

The US market is blaming Lloyd’s for irresponsibly chasing growth. E&S insurers are eyeing admitted insurers ramping up competition with frustration.

Cyclical fights and structural tug-of-wars

Some of these fights will resolve off in the middle distance when the market inflects upwards, like the internal broker fights and those between insurers and reinsurers. These are the cyclical flash points.

But the hard market also papered over some important structural cracks in the new industry structure.

The wholesalers made the lives of the retailers easy when placement became difficult, allowing them to focus on production and running lean operations.

But they are ultimately both chasing the same dollar of commission, and with the E&S market ballooning in size, retailers feel like too much value has been leached away.

How far the pendulum swings towards the retailers on commission will tell us something about the balance of power between these two parts of the value chain.

The retail/wholesale tension lessens in a rising market, but it doesn’t go away because the retailers are resentful of the E&S gatekeeping from the wholesalers.

The soft market will test the deconstructed insurance value chain, exposing weak MGA underwriting and opening the cracks in the highly leveraged fronting segment. (Re)insurers will absorb much of the loss.

But this structural problem remains even when rates rise.

Just as brokers have captured significant market value at the expense of carriers over the last 10-20 years, the deconstructed underwriting value chain is likely to further cannibalize value.

(Re)insurers will cede ground to the very ecosystem they helped build.

By Adam McNestrie

Request your free trial today to unlock our complete intelligence platform. ![]()

MGAs break free from the market cycle as new forces reshape the model

Read More

Market hardening is more than a reaction to headline-grabbing cat losses

Read More