-

Several airlines are understood to have come to market early.

Several airlines are understood to have come to market early. -

According to McKinsey, the projected spending on data centers is expected to hit $6.7tn by 2030.

-

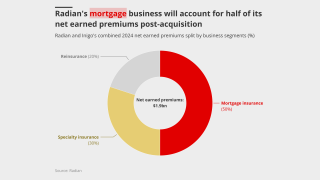

The deal will be watched closely by Radian’s handful of similar peers.

-

Small modular reactors are increasingly viewed as a means of meeting surging energy demand.

-

After losing in the High Court, insurers pin their hopes on the Court of Appeal.

-

Despite formation of Gabrielle, there is ‘a very high probability’ of a below-average season.

-

Part four looks at how the talent landscape will shift in response to AI introduction.

-

The low degree of overlap between the combining portfolios benefits both parties.

-

Organisations were challenged to address systemic DEI failure rather than play “word salad” with labels.

-

Property remains the dominant line, accounting for nearly 30% of total London premiums.

-

Plaintiffs allege that manufacturers and retailers have broken environmental laws.

-

From aviation claims to retention challenges, underlying dynamics will take time to play out.