Analysis

This analysis cuts straight to how a single satellite loss reset the space market. We show how the SpainSat event snapped a softening trend, reignited pricing discipline and exposed how fragile recent profitability really was. It delivers fast insight on rate momentum, the durability of new capacity and what this volatility means for underwriting power in a class where one loss can rewrite the year.

Subscribe to get comprehensive access to our exclusive analysis in the full platform.

Pricing pressure had begun to ease before the EUR352mn satellite total loss.

The space insurance market’s return to profitability has been thrown into question following a major early-year loss, reversing what had been shaping up as a period of stability for the class.

Market practitioners have told this publication that the SpainSat loss in early January has reversed the softening which was starting to take hold in the space insurance market, pushing rates back up just months after they were widely seen to have peaked.

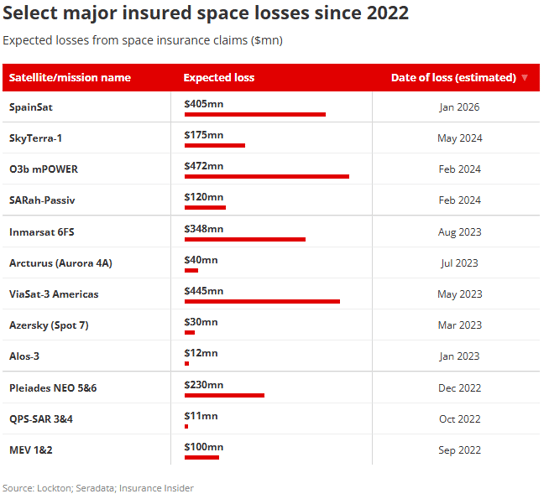

This publication revealed the Spanish military communications satellite had been notified as a EUR352mn ($405mn) total loss following damage sustained in orbit.

It came at a critical point in the space insurance market cycle, which, after several quarters of sharp rate increases driven by heavy losses in 2023 and 2024, had reached its high-water mark in 2025.

With rates returning to levels not seen since the early 2000s by late last year, coupled with improved results and a benign claims environment, pressure on pricing had begun to ease.

However, while there were reductions in some programmes as competition returned, that trend is understood to have been abruptly halted, with the SpainSat loss prompting an immediate reassessment of pricing.

The reversal highlights the fragility of the market’s recovery following one of the most severe corrections in its history.

Unlike other markets, the space market does not experience attritional losses. Rather, it suffers from high volatility, driven by severe, large, one-off losses which can impact a carrier’s whole year.

Business is also often placed six, 12 or even 24 months before the premium is earned.

This volatile structure is compounded by varying placement cycles, which can be anything from weeks to years.

Sources said the SpainSat event is expected to materially impact recent underwriting results, underlining the structural volatility of a class where a single loss can define a year’s performance.

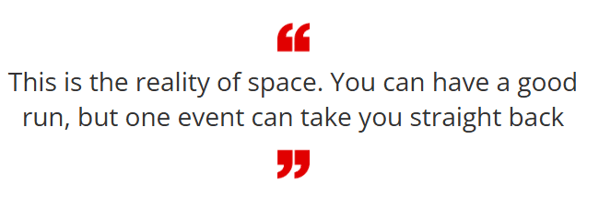

“This is the reality of space,” one market participant said. “You can have a good run, but one event can take you straight back.”

Market reached its apogee

Nearly $2bn of losses across 2023 and 2024 – against an annual premium base of roughly $500mn-$550mn – forced a dramatic repricing of risk, with rates rising by 50%, 100% and in some cases as much as 150%

By 2025, however, those higher-rated programmes were earning through, and claims activity had remained subdued, allowing underwriters to return to profitability and prompting a gradual reintroduction of competition.

In addition, overall claims for 2023 and 2024 also decreased by 2025, with Gallagher estimating these dropped from close to $2bn to $1.5bn.

The broker said in its latest Plane Talking report that the 20%+ decrease was driven primarily by an improving technical outlook on impaired satellites and underwriter settlement negotiations.

Increased competition

The timing of the major loss early in 2026 is significant given the competitive dynamics that had begun to re-emerge.

As this publication previously explored, the space market witnessed an exodus of capacity in the wake of the streak of major losses.

Over the course of 2023 to 2024, Canopius put its book into run-off, while Brit, Hiscox and Volante exited the market. Elsewhere, Munich Re scaled back its portfolio.

However, more recently the hardening market has attracted new interest in the class.

Hive entered the market with the hire of Jack Kenneally from Brown & Brown-owned Occam Underwriting and Whitecap Aerospace launched in the space insurance market with Tim Wright.

In addition, underwriters displaced by the withdrawals have since found new homes, with the ex-Hiscox team and the former Volante team resurfacing as Phemis and Aesir Space respectively.

Sources said ample capacity and improved profitability had led to increased competition for well-performing risks, with some underwriters struggling to secure meaningful lines as others sought to grow their books.

That dynamic is now in question, at least in the near term.

Despite the setback, there is no immediate indication of capacity withdrawing from the class. Capital providers remain broadly supportive, and the structural improvements achieved through recent repricing are still intact.

However, the SpainSat loss underscores the extent to which recent profitability had been supported by a period of unusually low claims activity, rather than a fundamental change in the risk profile.

Broader structural challenges also persist. Demand remains concentrated in a relatively small number of high-value GEO satellites, while the pipeline continues to shift towards newer technologies.

At the same time, insurance penetration across ‘New Space’ segments such as SpaceX remains limited, constraining diversification and leaving the market exposed to large, individual losses.

For now, market participants said the focus will return to pricing discipline, technical underwriting and the performance of satellites currently progressing through critical mission phases.

By Rebecca Perkins

19 March, 2026

Request your free trial today to unlock our complete intelligence platform. ![]()

-1.jpg?length=360&name=download%20(3)-1.jpg)

Syndicate‑in‑a‑box: Useful stepping‑stone or failed experiment?

Read More

M&A year in review: Lloyd’s activity ramps up, PE-backed broker sales slow

Read More.png?length=360&name=Feature%20image%20(sharing%20size).png)