Analysis

This analysis piece shows how Insurance Insider ILS helps subscribers spot and assess a potential new growth avenue for ILS capital. It explains why surging data centre investment is creating outsized limit demand, where traditional insurance capacity may fall short, and how ILS structures from collateralised reinsurance to cat bonds could step in. The article cuts through the hype by highlighting real obstacles around modelling, contents valuation and business interruption, giving readers a clear view of what must be solved before data centre risk becomes a scalable opportunity.

Subscribe to get comprehensive access to insight, analysis, opinion and more across the full platform.

A single data centre campus can require more than $10bn in insurance limits, according to Aon.

ILS managers have discussed options for data centre risk transfer with potential sponsors and brokers, including how to value building contents within a data centre campus, sources told Insurance Insider ILS.

Initial conversations have focused on catastrophe risk structured as collateralised reinsurance deals, with cat bonds also potentially in scope within a couple of years.

The potential sponsors include insurance firms writing primary market covers for the centres and banks providing financing to data centre developers for construction and development projects.

The perils in scope are severe convective storm (SCS), flood, quake and wildfire, as well as cyber.

Analysis by broker Aon estimated that a single data centre campus can require more than $10bn in insurance limits and therefore requires “substantial reinsurance and third-party capital”.

Euler ILS is among managers scoping (re)insurance carriers with a view to providing catastrophe cover through a collateralised quota share structure.

Niklaus Hilti, CEO of Euler ILS, said: “Our ambition is to start towards $1bn of cat coverage for data centres, but that can be scaled up relatively quickly.”

Other ILS managers have held exploratory conversations with insurance carriers to scope potential deals, including whether these would be structured as standalone transactions or as part of a broader portfolio quota share.

Sources note a preference to support a portfolio of data centres underwritten by a single corporate, rather than a single facility, due to increased diversification benefits.

Richard Pennay, CEO of Aon Securities, said: “It’s more efficient in the short term to provide capacity on a portfolio of data centres rather than an individual data centre.”

Data centre bonds could start with parametric triggers

Sources said the first data centre cat bond could be issued within two years and would likely be structured with a parametric trigger.

Adil Imani, director of ILS at Verisk, said parametric structures offered a good starting point for managers, enabling them “to build confidence in the modelled loss outputs”, including around data centre contents.

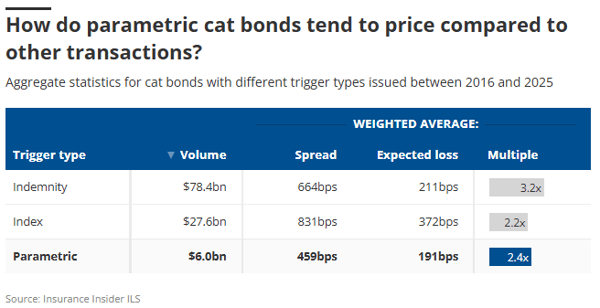

Bonds with parametric triggers have made up around 5% of total issuance volumes over the past 10 years.

These parametric deals have offered investors a lower multiple on expected loss, on a weighted average basis, at 2.4x, compared to indemnity bonds at 3.2x.

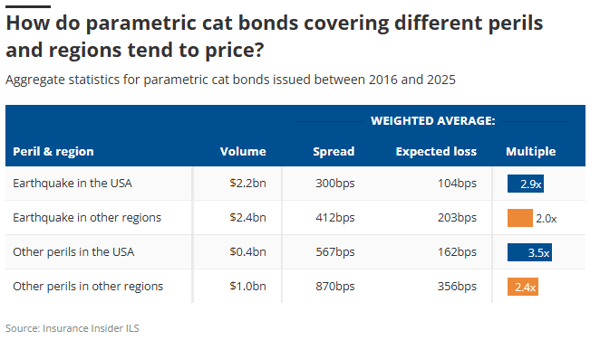

This partly reflects the strength of appetite for diversifying quake deals – where structures commonly have parametric triggers – including from UCITS funds whose rules require a certain proportion of diversifying investments.

Analysis of parametric bond pricing by Insurance Insider ILS indicates that for US perils other than quake, the average multiple at 3.5x is higher than for indemnity bonds.

This is partly due to concerns about the level of basis risk that can be a feature of deals with a parametric trigger.

One ILS manager noted that sponsors could look to design a trigger for data centre bonds that would narrow down the exposure to focus on the centre’s specific location, reducing the amount of basis risk in the deal.

This could involve using a data centre’s own sensors to determine if a bond has attached, giving a more granular basis for the trigger.

For quake, sensors can measure ground acceleration, or for tornadoes, the track within the campus, rather than relying on US government sensors located further away.

There is also potential for indemnity bond deals to follow, once investors have a better grasp of data centre risk.

“There is no reason why the cat bond market wouldn’t be able to provide indemnity-based protection for data centres,” Pennay said.

“As long as the transactions are structured and modelled well, we expect cat bond investors to have a propensity and willingness to assume this exposure,” he said.

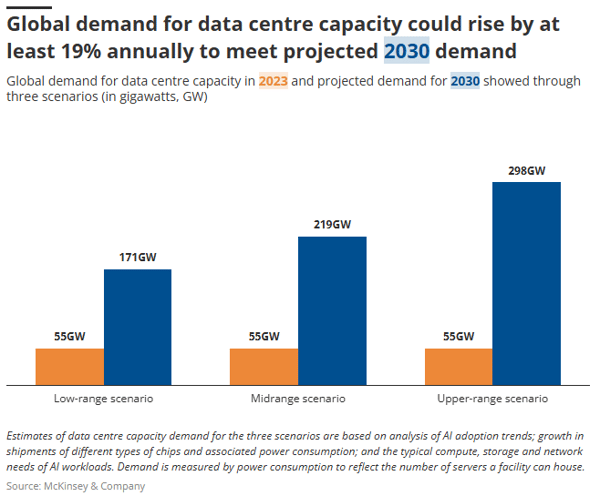

Aon estimated there will be $5tn-$10tn of spending on data centre construction over the next five years.

Using gigawatts as a proxy for data centre capacity, the broker estimates growth of at least 19% annually to meet demand by 2030.

Insurance premiums are expected to reach a cumulative $134bn from 2026-2030, the broker added.

Processing chips are difficult to value

A key discussion point for ILS managers and potential sponsors is how to model and value the contents of a data centre, specifically the processing chips.

Derek Blum, senior director of product management at Moody’s, said: "Contents make up 50%-75% of a data centre's total value today, up from 30%-50% a few years ago."

One ILS manager said they discussed providing collateralised reinsurance capacity for data centres with certain insurance counterparties at the 1 January renewals.

However, they opted against investing due to concerns about modelling and valuing the contents.

Processing chips are often expensive and have a limited shelf life, meaning their value can depreciate precipitously.

Nvidia processing chips used in data centres have a typical shelf life of one to three years due to the heavy processing requirements.

Within a given data centre, more expensive chips will often exist alongside older, less valuable chips, which creates challenges in arriving at accurate valuations, potentially leaving investors over-exposed, sources said.

Risk mitigation at data centres can also significantly impact on exposures.

Raising chips by a few inches above ground level could materially reduce flood exposure, sources noted.

Similarly, if chips are stored individually in protective casing, this limits the risk of full or partial loss from a wildfire event.

Business interruption is a potential loss

Another major loss consideration, which is expected to become more prevalent once data centres are operational, is business interruption (BI), sources said.

One modelling source argued that BI losses would be limited due to data centres having good back up arrangements in place.

However, Imani said: “BI losses can compound really quickly and even exceed losses to the building and contents.”

A data centre BI loss could be triggered by a natural catastrophe event hitting an energy substation several miles away from the facility itself.

One source said: “You care about the impact of an event on the data centre, but also about the accumulation and aggregation of losses across all the connected facilities.”

Potential SCS impacts to data centres are also a concern for investors, given the concentration of data centres in the US Midwest and the rising losses associated with SCS and the tornado sub-peril in the region.

According to Aon Catastrophe Insight, SCS was the single most costly cat peril globally over the five-year period 2020-2025, causing $794bn of insured losses, ahead of tropical cyclone at $785bn.

Gallagher Re estimated SCS accounted for $60bn of the total $129bn in global insured cat losses last year.

By Jai Singh

16 March, 2026

Request your free trial today to unlock our complete intelligence platform. ![]()