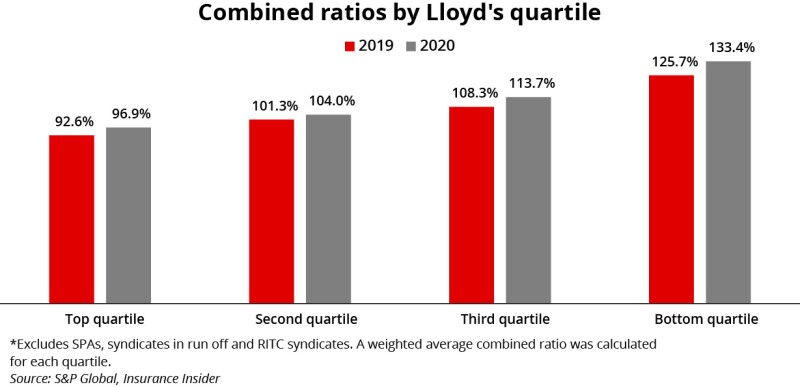

The best-performing quartile of syndicates at Lloyd’s outperformed the market aggregate combined ratio by 13.4 points in 2020, analysis by Insurance Insider has found.

The top quartile of syndicates reported a weighted average combined ratio of 96.9%, compared with the Lloyd’s market result of 110.3%.

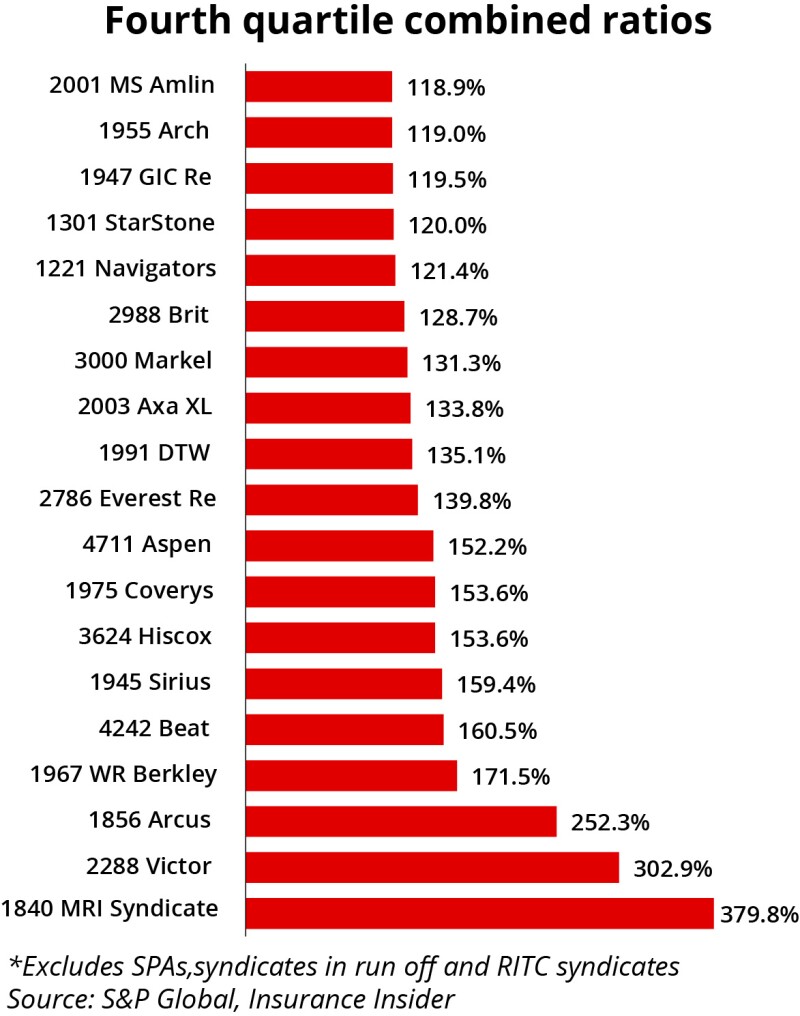

At the other end of the spectrum, the worst-performing quartile in the market underperformed the Lloyd’s market average by 23.1 points, with a weighted average combined ratio of 133.4%.

In a year where the impact of Covid-19 was felt unevenly across the market – largely depending on a syndicate’s exposure to event cancellation and other Covid-impacted classes – the range of 2020 combined ratios in Lloyd’s from the best to the worst performer is wider than in past years. This year there is a spread of 341.0 percentage points, or 213.5 points when excluding new launches Victor 2288 and Munich Re Innovation Syndicate 1840 from the bottom of the ranking.

This compares with a spread of 111.0 points in 2019 and 187.2 points in 2018.

However, the range of combined ratio results also demonstrates the challenge the Corporation faces in trying to remediate a market which diverges greatly on performance, with poorer performers still bringing down the average result and some posting ongoing losses. The Lloyd’s 2020 market results did, however, show an improvement on an underlying basis, with the attritional loss ratio shrinking 5.4 points as a result of the remedial work and improved rate.

In total, 64% of Lloyd’s syndicates reported an underwriting loss in 2020, according to Insurance Insider figures.

A deep-dive analysis of individual syndicate accounts has allowed this publication to rank 2020 performance by quartile, with the full ranking of syndicates published at the bottom of this article.

To achieve a more accurate representation of live syndicate performance in 2019, this analysis excludes syndicates in run-off as of 1 January 2020, reinsurance-to-close syndicates and quota share special purpose arrangements (SPAs) without their own underwriting teams.

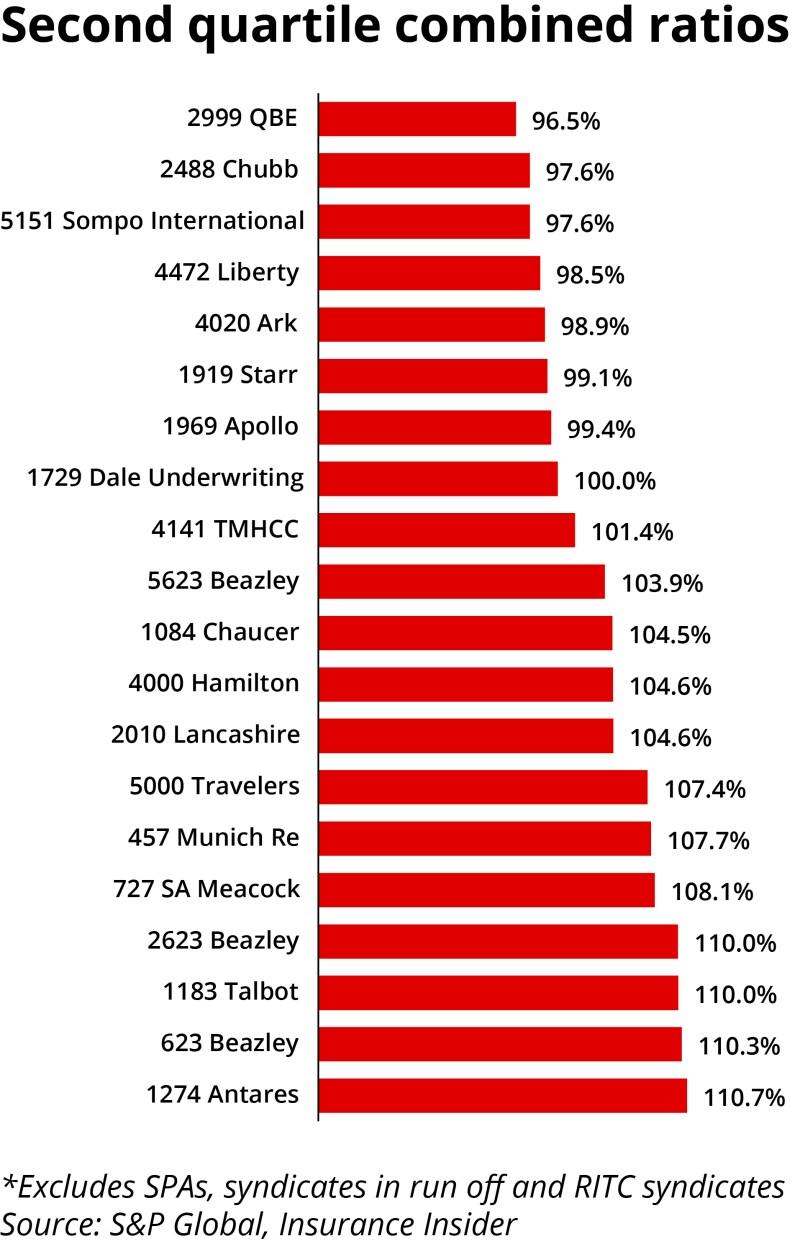

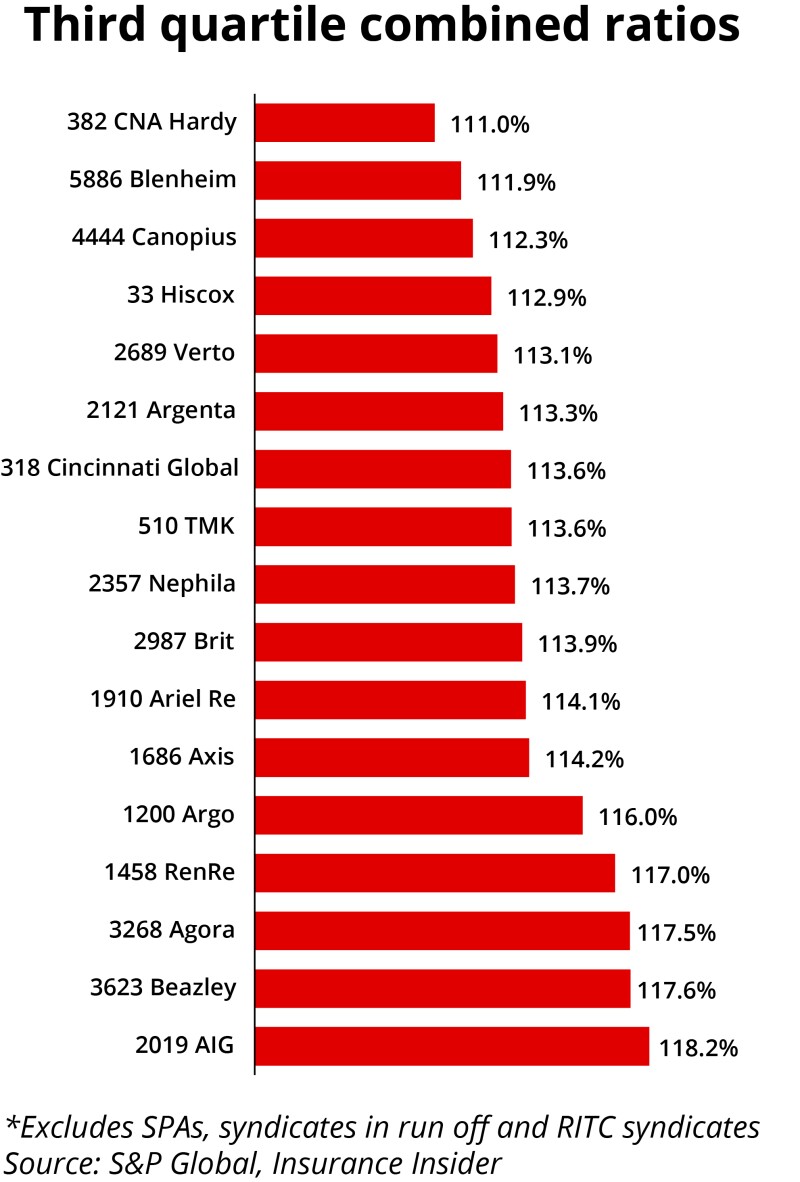

In our analysis, all quartiles reported a worse average combined ratio result compared with 2019, however, the extent of the year-on-year deterioration grows as you move down the quartiles.

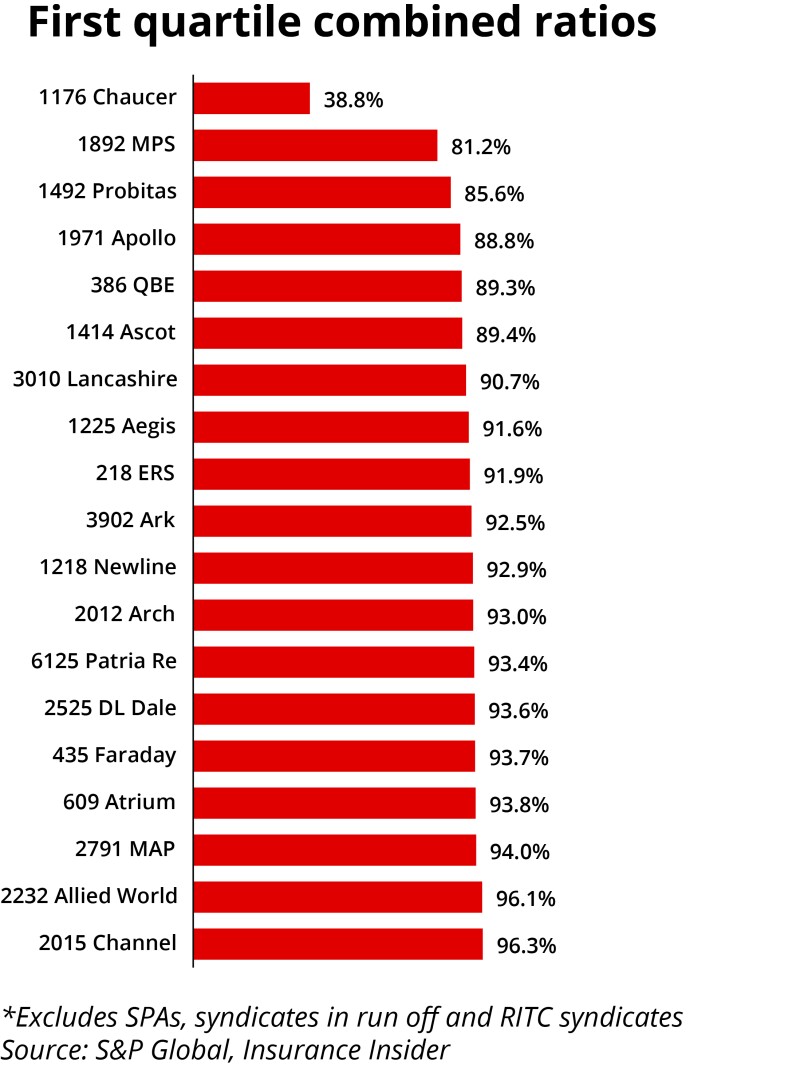

Some of the best performers in the top quartile specialise in lines less impacted by Covid-19 in 2020, such as the Medical Protection Society Syndicate 1892, liability-focused DL Dale 2525 and QBE Casualty Syndicate 386.

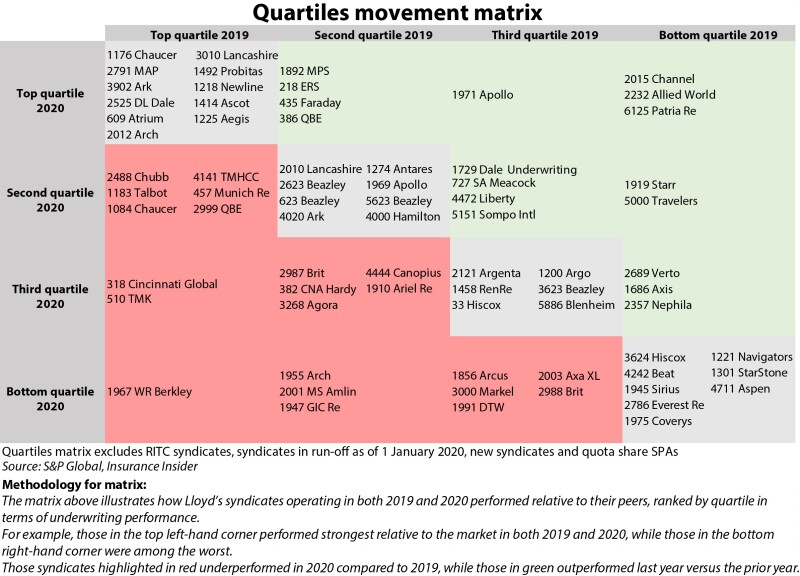

Our matrix below shows the movement of syndicates between quartiles from 2019 to 2020.

As the matrix shows, top-quartile performers also tended to be the most consistent in their underwriting performance from year to year, even in a 2020 that was heavy on both Covid claims and catastrophes. A total of 11 syndicates that were in the top quartile for 2019 stayed in that quartile for 2020.

Many of this subset of consistent top-quartile performers are also light-touch syndicates, which are afforded automatic plan approval due to a track record of outperformance. These include Aegis 1221, Atrium 609, MAP 2791, DL Dale 2525, and Ascot 1414.

It is understood that Lancashire 3010, led by Lancashire Syndicates CEO Emma Woolley, is also a light-touch syndicate, although to date this has not previously been reported.

Chaucer’s nuclear syndicate 1176 is also a perennial outperformer with a combined ratio of 39%.

Probitas 1492, not a light-touch syndicate, is also in its second year of top-quartile status after turning its first underwriting profit in 2018 following remediation work. The syndicate delivered a nine-point improvement in its combined ratio year on year to 86%.

Active underwriter Ash Bathia said in the syndicate’s accounts that it closed the 2018 year of account with an 89.8% combined ratio and expected the 2019 year of account to run at 86.3%. The 2020 year of account is forecast at 87.8%.

“Our team is looking forward to building further on these strong foundations to deliver another positive performance in 2021 against the backdrop of favourable market conditions and establishing a high calibre managing agency with robust governance and compliance framework,” he said.

Biggest improvers

Some of the biggest combined ratio improvements in the market have led those syndicates to jump up a quartile or more.

Patria Re 6125 made a 34-point improvement in the year to take it from the bottom quartile in 2019 to the top quartile for 2020, as a result of fewer large cat losses in 2020 compared with the previous year. The lower level of cat losses managed to offset the syndicate’s Covid impact, which was equivalent to 6.8% of net earned premium.

However, 2020 was Patria Re’s last year of performance after management took the decision to close the syndicate for 2021. Management said this was driven by concerns that it was unlikely that the syndicate would produce an adequate return on capital.

Both Allied World 2232 and Channel 2015 also made the jump from the bottom quartile to the top, with year-on-year improvements of 25 points and 17 points, respectively.

Allied World said the 2020 loss ratio at Syndicate 2232 benefitted from a lower level of cat losses compared with 2019, when it took a hit from Japanese wind losses. The syndicate also released reserves for 2020, compared with a reserve charge taken in 2019. Meanwhile, the syndicate had a low level of exposure to Covid-19, taking just a £2mn net loss from the event in 2020.

Meanwhile, 2020 marked a return to profitability for Channel 2015, with a combined ratio of 96%. The syndicate has been hard at work turning around performance, and is also seeing the benefits of an RITC transaction for the 2017 and prior years, which has worked to stem adverse prior-year development.

Biggest deteriorations

At the other end of the spectrum, similarly some of the largest deteriorations in combined ratio led to syndicates falling down the quartiles.

The starkest example here was WR Berkley 1967, where the combined ratio surged 83 points year on year to 171%, as the pandemic impacted the business across multiple underwriting years, primarily on contingency business. The result moved the syndicate from the top quartile in 2019 to the bottom in 2020.

Excluding Covid-19 losses, the syndicate result would have been a profit of $29.5mn with a combined ratio of 88%, according to the syndicate’s annual report. Future losses from the contingency book as a result of Covid-19 have also now been capped via a loss portfolio transfer with Berkley Insurance Company.

Arcus 1856 is the worst-performing mature syndicate in the ranking for 2020, with Victor 2288 and Munich Re Innovation Syndicate 1840 – which posted weaker combined ratios – still in their first year of operation and not yet at critical mass to outweigh expenses.

In its annual report, Arcus said its 252% combined ratio was partly due to several medium-sized cat losses – in particular hurricanes Laura and Sally, the Iowa derecho and the Alberta hailstorm – that came below the attachment point of their outwards protection and therefore taken net.

The net combined ratio was also heavily affected by a £49mn premium transfer to Arch Syndicate 1955, in relation to the commutation of a whole account quota share on the 2017 and prior years of account. Without this transfer, the combined ratio would be at 134%, Arcus said.

Arcus has now come under new ownership after its acquisition by ERS. The syndicate was effectively saved at the 11th hour after Credit Suisse indicated that it wished to scale back or entirely discontinue its support of the business.

Some syndicates also deepened their losses and their position in the fourth quartile.

The combined ratio at Aspen 4711 – the worst-performing syndicate in 2019 – deteriorated by 13 points year on year to 152% as a result of reserve strengthening and Covid-19 losses predominantly arising from accident and health, which Aspen 4711 exited as a class earlier in 2020, alongside marine liability.

As part of ongoing remediation efforts, Aspen Group last March secured an adverse development cover providing $1bn in coverage through Enstar, in which the syndicate also participates.

Meanwhile, Sirius 1945 also deepened its underwriting losses year on year, with a 39.1-point worsening in the combined ratio to 159%. The surge in the loss ratio was largely down to Covid-19 claims, a significant portion of which related to losses attaching to the 2018 and prior underwriting years of account on its discontinued contingency book.

Pandemic related losses at Sirius 1945 were £57mn, adding 58 points to the 2020 combined ratio.

At Beat 4242, it was cat activity that brought the deterioration of the underwriting performance, as it took a string of losses though the Icat portfolio. The 2020 combined ratio of 161% was a 41-point deterioration on the previous year.

“Every mile of the mainland US Atlantic coast, from Texas to Maine, was under a watch or warning related to tropical cyclones at some point in 2020. Only five counties avoided tropical storm-force winds. Away from the coasts, heightened activity arising from the so-called secondary perils such as tornadoes and wildfires, including the derecho event which swept through the Midwest in August also impacted the result,” active underwriter Tom Milligan wrote in the annual report.

The syndicate has discontinued all underwriting through Icat Managers in 2021, substantially reducing its exposure to US catastrophe events.

In its place, the principal areas of growth are alternative risk insurance, D&O insurance, specialty and proportional reinsurance, and property insurance with a restricted catastrophe appetite, Milligan said.

See below for all full, live syndicates ranked by combined ratio.