Analysis

What actually causes the property insurance market to harden? It's not simply the scale of catastrophe losses, but the macroeconomic backdrop, and short-term interest rates in particular, that often decides whether pricing turns. This analysis shows how some of the largest hurricanes on record failed to harden pricing while smaller events did, why property pricing tracks interest rates through capacity, inflation and mark-to-market pressure on carriers' assets, and how ILS complicates the usual capacity crunch. It delivers fast insight on the interest-rate signals worth watching alongside the hurricane forecasts, and what current rate forecasts could mean for conditions at the next January renewal.Subscribe to get comprehensive access to our exclusive analysis in the full platform.

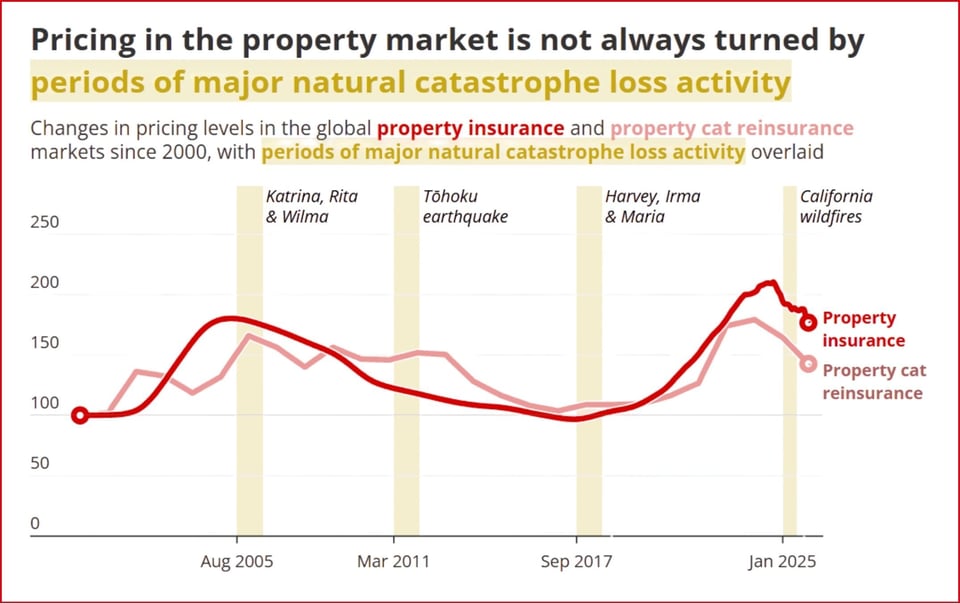

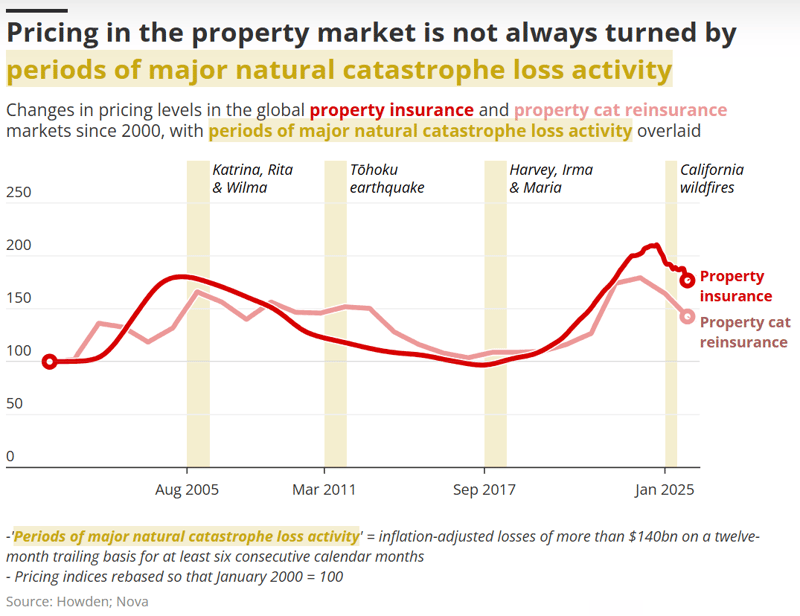

The property pricing cycle correlates strongly with interest rates.

Underwriters and brokers tend to talk about market cycles in relation to major cat or other significant loss events.

Hardening after 9/11 in 2001 and the trio of 2005 hurricanes – Katrina, Rita and Wilma – are classic examples of the way vast storms or outsized manmade disasters can create a spike in property or even broader P&C pricing, sometimes lasting for two or three annual renewals.

But at times, even enormous cat losses are not enough to turn the market or slow the decline of pricing.

Data collated by Howden Re bears out the theory. Hurricanes Harvey, Irma and Maria, which struck in the depths of the soft market in 2017, caused only limited hardening in cat and property pricing.

Likewise, 2018’s Florence and Michael also had some hardening impact – but it wasn’t until three years later that rates took a dramatic upward turn.

The key to understanding when a cat event sparks a hard market and when it doesn’t, the Howden Re data suggests, is to look at the broader macroeconomic picture that accompanied that event.

The timeline above shows that rates truly began to harden in 2020, as the Covid pandemic caused a major global economic shock.

The after-effects of Covid, as the world’s major economies struggled with the costs of lockdown measures, formed the backdrop to further hardening in 2021 and 2022.

During that period, (re)insurers also had to contend with Hurricane Ida in 2021 and Hurricane Ian in 2022, the latter of which racked up $67bn in losses.

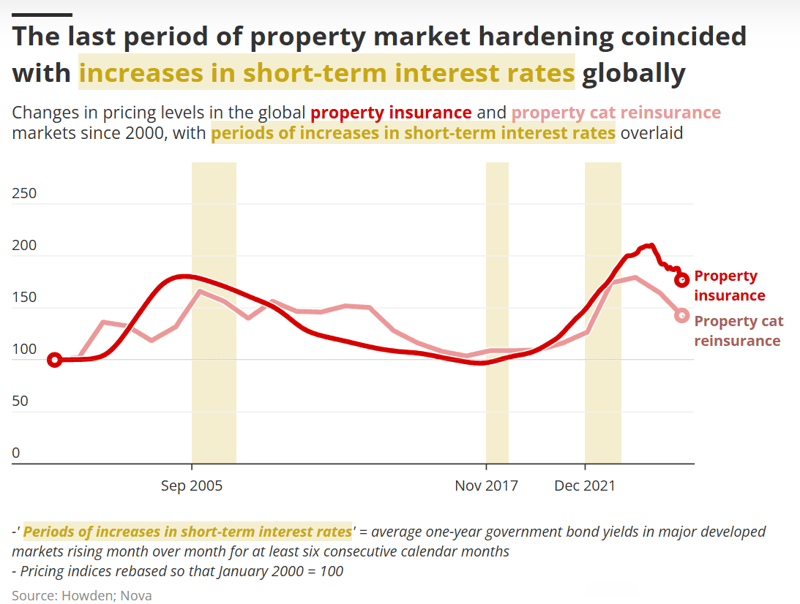

Howden Re’s data suggests that property pricing is also contingent on the fluctuations of short-term interest rates.

As shown in the chart below, while there is often an insurance pricing reaction to years in which major losses climb towards $100bn, hardening also correlates with spikes in interest rates.

When interest rates start to rise, capital quickly flows towards safer assets, with reduced investor appetite for activity including cat reinsurance. That leads to a sharp contraction in traditional (re)insurance capacity.

At the same time, interest rates also tend to coincide with inflation, as raising them is a key tool of central banks designed to cull runaway prices – and inflation drives up loss costs for insurers.

Rising interest rates also hit carriers’ fixed income assets, resulting in mark-to-market losses as seen in the aftermath of the 2020 Covid-related market rout.

All of these elements put pressure on carriers to raise rates.

The experience of 2022 illustrates the concept. In 2022, as interest rates rose following the shock of the Ukraine war, aggregate reinsurance capital shrank, data from Gallagher Re shows.

The experience of 2022 illustrates the concept. In 2022, as interest rates rose following the shock of the Ukraine war, aggregate reinsurance capital shrank, data from Gallagher Re shows.

Accordingly, the 2023 property treaty renewals were a step-change for reinsurers, who secured double-digit rate increases, tightened terms and conditions and increased attachment points – the latter of which have yet to unwind.

The reinsurance market is currently awash with capacity, which has contributed to the reduction in property cat rates seen at 1 January, 1 April and 1 June so far this year.

A complicating factor is the macro environment’s influence on ILS participation. The pattern here is not so straightforward.

Many participants choose to invest based on the value of ILS relative to other assets, so if an ILS play is favourable to other investments, ILS capacity can grow even when interest rates rise. This can have a dampening effect on the traditional capacity crunch.

At this point in the year, as market participants attempt to predict conditions at the next January renewal, attention typically turns to the North Atlantic hurricane season forecasts, which currently describe a quieter than average season.

But it may also be prescient to look to short-term interest rate forecasts as well to determine likely conditions.

The Organisation for Economic Cooperation and Development has charted short-term interest rates falling to 2.8% in 2025 from 3.7% in 2024 in the Euro area, and to 4.1% from 5.1% in the US over the same period.

These declines followed sharp increases from 2021 onwards.

However, the European Central Bank, the Bank of England and the US Federal Reserve have all indicated potential interest rate increases this year as they look to counter inflation caused by the impact of the Middle Eastern conflict on energy prices.

The interest rate environment has yet to have had a profound impact on the supply of capacity and insurers’ willingness to write business at present, with reinsurance sources reporting no signs that softening will slow at 1 January next year.

As global economies look to counter the impacts of geopolitical conflicts and the energy crisis, however, interest rates could become a mitigating factor to the overall excess of capacity in future.

By Rachel Dalton, Ben Wylie

24 June, 2026

Request your free trial today to unlock our complete intelligence platform. ![]()

MGAs break free from the market cycle as new forces reshape the model

Read More

Will State Farm’s AI discrimination suit break the regulatory dam?

Read More